Trade Negotiations; Damage to Iran’s Nuclear Capabilities

7/7/2025 - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

Continued growth in the economy will boost earnings, with earnings of U.S. multinationals receiving an extra boost from the roughly -7.1% decline in the value of the U.S. dollar over the course of 2Q 2025 through the currency translation effect, providing the necessary support for higher stock prices. Taken with successful negotiations leading to a series of trade deals which would go a long way toward calming the fears of investors and consumers and providing businesses with some clarity on the rules of the road going forward, investors will be rewarded by thinking about what could go right, rather than about what could go wrong.

Based on the timing of President Trump backtracking on tariffs and announcing policy accommodations over the past three months, markets have concluded that the worst of the proposed tariffs is very unlikely to come to fruition. It is clear the Administration is paying close attention to how the financial markets and economic participants respond to his tariff proposals. The significant potential economic damage is not politically palatable, as the electorate did not vote for a recession or continued elevated inflation.

The announcement of the reciprocal tariffs on April 2 provided investors with a glimpse of the worst possible impact on the economy from the tariffs, while the reaction in stocks and bonds gave an indication of the possible downside risks to the markets. The longer the oppressive tariff rates would have remained in place, the greater the likelihood of recession would have grown, and the more the potential severity of the recession would have increased.

Investor sentiment received a boost on June 5 following the announcement that President Trump and Chinese leader Xi held a long awaited phone call, which concluded with an agreement to hold a second round of high level trade talks in London. China and the U.S. repeatedly accused each other following the May 10-11 trade talks of violating the Geneva agreement as the trade conflict veered away from tariffs to each country’s export controls on materials and products the other side critically needs.

Equity Markets

China Trade Negotiations, Serious Damage to Iran’s Nuclear Capabilities

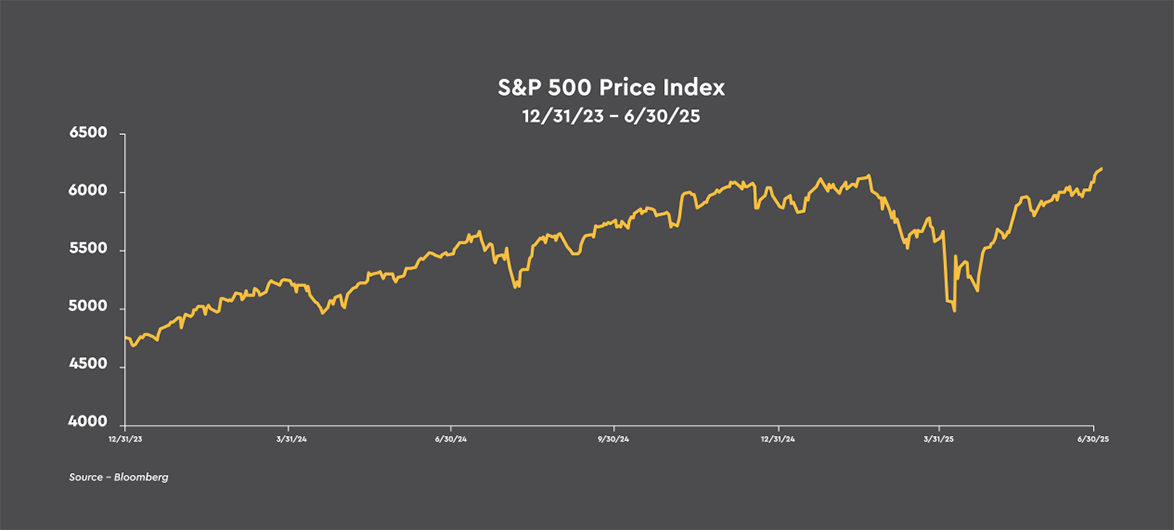

The rebound in common stock prices off the recent April 8 low continued into early June as investors focused on what they believed would be the most likely outcomes for the tariff-related trade conflicts and the path forward for the economy. It is increasingly expected that a series of bilateral trade deals with the major trading partners of the U.S. will be announced over the summer months. The economy’s growth rate is expected to slow from the hit to both consumer and business sentiment from the tariff threats, but skirt a recession with the easing trade tensions, and possibly accelerate over the back half of the year and into 2026 as the tax and spending bill is completed, efforts to further roll back regulations progress, and the Fed likely cuts interest rates.Based on the timing of President Trump backtracking on tariffs and announcing policy accommodations over the past three months, markets have concluded that the worst of the proposed tariffs is very unlikely to come to fruition. It is clear the Administration is paying close attention to how the financial markets and economic participants respond to his tariff proposals. The significant potential economic damage is not politically palatable, as the electorate did not vote for a recession or continued elevated inflation.

The announcement of the reciprocal tariffs on April 2 provided investors with a glimpse of the worst possible impact on the economy from the tariffs, while the reaction in stocks and bonds gave an indication of the possible downside risks to the markets. The longer the oppressive tariff rates would have remained in place, the greater the likelihood of recession would have grown, and the more the potential severity of the recession would have increased.

Investor sentiment received a boost on June 5 following the announcement that President Trump and Chinese leader Xi held a long awaited phone call, which concluded with an agreement to hold a second round of high level trade talks in London. China and the U.S. repeatedly accused each other following the May 10-11 trade talks of violating the Geneva agreement as the trade conflict veered away from tariffs to each country’s export controls on materials and products the other side critically needs.

Investor sentiment received a boost on June 5 following the announcement that President Trump and Chinese leader Xi held a long awaited phone call, which concluded with an agreement to hold a second round of high level trade talks in London.

When U.S negotiators sat down with their Chinese counterparts on June 9-10, they pressed Xi Jinping’s representatives to speed up exports of rare earth minerals and magnets which are critical for the automotive, manufacturing, and defense sectors. China mines roughly 60% of the world’s rare earth minerals and processes almost 90% of them. However, China only agreed to a six month extension on rare earth and magnet export licenses, allowing Beijing to retain its chokehold on critical minerals and magnets and giving Beijing leverage to easily escalate trade tensions again while adding to uncertainty for U.S. companies.

Chinese negotiators pushed Washington to relax some recent restrictions on the sale of jet engines and related parts, curbs on semiconductor chip design software, and student visas. Washington also agreed to remove a new restriction on ethane sales, a by product of natural gas and oil drilling, which China relies upon for its petrochemical manufacturing.

The stakes were high for the global economy in the London negotiations as the export restrictions imposed by the two nations were impacting supply chains by disrupting the worldwide flow of goods, raw materials, and components. Negotiating trade deals with China is a challenge as it has effectively leveraged its industrial policy -- including export controls, currency manipulation, manufacturing sector subsidies, low environmental standards, and forced technology transfers -- to solidify its strategic positioning.

Chinese negotiators pushed Washington to relax some recent restrictions on the sale of jet engines and related parts, curbs on semiconductor chip design software, and student visas. Washington also agreed to remove a new restriction on ethane sales, a by product of natural gas and oil drilling, which China relies upon for its petrochemical manufacturing.

The stakes were high for the global economy in the London negotiations as the export restrictions imposed by the two nations were impacting supply chains by disrupting the worldwide flow of goods, raw materials, and components. Negotiating trade deals with China is a challenge as it has effectively leveraged its industrial policy -- including export controls, currency manipulation, manufacturing sector subsidies, low environmental standards, and forced technology transfers -- to solidify its strategic positioning.

Negotiating trade deals with China is a challenge as it has effectively leveraged its industrial policy -- including export controls, currency manipulation, manufacturing sector subsidies, low environmental standards, and forced technology transfers -- to solidify its strategic positioning.

However, China’s current economic woes -- persistent deflationary influences, sluggish domestic demand, a rising unemployment rate, and a residential real estate crisis -- were strong incentives for China to strike a workable trade deal with the U.S. The trade deal negotiated in London resulted from each side’s leverage over the other, not from common principles or shared interests.

The advance in common stock prices was temporarily interrupted mid-month after Israel launched a massive series of air strikes against Iran, aimed at crippling its nuclear enrichment program, degrading its ballistic missile program, and killing senior military leaders and nuclear scientists. The air strikes were ordered after Iran showed signs of accelerating its nuclear progress, taking steps to weaponize its nuclear material. The Israeli strikes seriously damaged Iran’s nuclear program and achieved air supremacy over Iran.

The immediate response in the markets was a one day return to risk-off sentiment with the S&P 500 falling -1.1%, just as the S&P 500 was 1.6% away from reaching its all-time record high. Oil prices initially rose sharply, rising as much as 14% in the aftermath of the air strikes, before closing a little more than 7% higher on June 13. However, oil prices stabilized over the next few days as Iran’s oil infrastructure was not targeted and the Strait of Hormuz -- through which roughly 20% of daily worldwide oil production flows -- remained open.

Nine days after Israel struck Iran’s nuclear facilities, the U.S. decisively entered into the conflict with Iran when the Trump administration came to believe Iran was not ready to strike a satisfactory nuclear deal after European leaders met with their Iranian counterparts in Geneva on June 20. The conclusion was that U.S. military force was necessary to take out Iran’s highly fortified nuclear facilities with Iran fast approaching a point of no return in its quest to obtain nuclear weapons.

The U.S. unleashed airstrikes on the most protected targets in Iran’s nuclear program, using stealth bombers and bunker-busting bombs to seriously damage key nuclear facilities. So far, the markets are viewing the attacks on Iran by Israel and the U.S. from a positive perspective given Iran’s severely degraded military capability which means there is little, or no, chance of retaliation against the U.S. or Israel by Iran in the near future.

Additionally, given the weakened state of Iran’s economy, it is extremely unlikely Iran will attempt to disrupt oil flows through the Straight of Hormuz as it would eliminate a significant source of oil revenue for the Iranian economy. Given the extent to which China has influence on Iran’s economy -- a great deal of Iran’s oil is sold to China -- and geopolitical standing, it also does not make sense that Iran would do anything to disrupt the flow of oil to China from the Strait.

Dampened Middle East tensions drove a renewed risk-on sentiment as June drew to a close, helped by Presidents Trump’s announcement of a ceasefire between Israel and Iran. Even prior to the ceasefire announcement, markets responded positively to the U.S. airstrikes on Iranian nuclear facilities, the lack of disruption to oil flows from the Middle East, Israel’s Prime Minister saying Israel was “very, very close” to achieving its war aims, and Iran launching a relatively small barrage of 14 missiles against the largest U.S. military base in the Middle East in retaliation to the U.S. airstrikes, and only after sending prior warning to authorities in Qatar.

The limited Iranian counterattack was a calculated response which provided an off ramp to further conflict that avoided more hostile steps such as closing the Strait of Hormuz or direct ship-to-ship attacks. Oil prices retreated and stock prices climbed after Iran’s response avoided striking critical energy infrastructure, easing fears that the Middle East conflict would roil oil markets.

Oil prices are the key data point to watch as oil is the primary conduit through which other market prices will react. To keep a lid on oil prices, it is crucial that no disruption to oil flows through the Strait of Hormuz takes place. A super spike in oil prices above $100 per barrel would have a negative impact on the global economy and likely lead to a significant drop in global stock prices.

The advance in common stock prices was temporarily interrupted mid-month after Israel launched a massive series of air strikes against Iran, aimed at crippling its nuclear enrichment program, degrading its ballistic missile program, and killing senior military leaders and nuclear scientists. The air strikes were ordered after Iran showed signs of accelerating its nuclear progress, taking steps to weaponize its nuclear material. The Israeli strikes seriously damaged Iran’s nuclear program and achieved air supremacy over Iran.

The immediate response in the markets was a one day return to risk-off sentiment with the S&P 500 falling -1.1%, just as the S&P 500 was 1.6% away from reaching its all-time record high. Oil prices initially rose sharply, rising as much as 14% in the aftermath of the air strikes, before closing a little more than 7% higher on June 13. However, oil prices stabilized over the next few days as Iran’s oil infrastructure was not targeted and the Strait of Hormuz -- through which roughly 20% of daily worldwide oil production flows -- remained open.

Nine days after Israel struck Iran’s nuclear facilities, the U.S. decisively entered into the conflict with Iran when the Trump administration came to believe Iran was not ready to strike a satisfactory nuclear deal after European leaders met with their Iranian counterparts in Geneva on June 20. The conclusion was that U.S. military force was necessary to take out Iran’s highly fortified nuclear facilities with Iran fast approaching a point of no return in its quest to obtain nuclear weapons.

The U.S. unleashed airstrikes on the most protected targets in Iran’s nuclear program, using stealth bombers and bunker-busting bombs to seriously damage key nuclear facilities. So far, the markets are viewing the attacks on Iran by Israel and the U.S. from a positive perspective given Iran’s severely degraded military capability which means there is little, or no, chance of retaliation against the U.S. or Israel by Iran in the near future.

Additionally, given the weakened state of Iran’s economy, it is extremely unlikely Iran will attempt to disrupt oil flows through the Straight of Hormuz as it would eliminate a significant source of oil revenue for the Iranian economy. Given the extent to which China has influence on Iran’s economy -- a great deal of Iran’s oil is sold to China -- and geopolitical standing, it also does not make sense that Iran would do anything to disrupt the flow of oil to China from the Strait.

Dampened Middle East tensions drove a renewed risk-on sentiment as June drew to a close, helped by Presidents Trump’s announcement of a ceasefire between Israel and Iran. Even prior to the ceasefire announcement, markets responded positively to the U.S. airstrikes on Iranian nuclear facilities, the lack of disruption to oil flows from the Middle East, Israel’s Prime Minister saying Israel was “very, very close” to achieving its war aims, and Iran launching a relatively small barrage of 14 missiles against the largest U.S. military base in the Middle East in retaliation to the U.S. airstrikes, and only after sending prior warning to authorities in Qatar.

The limited Iranian counterattack was a calculated response which provided an off ramp to further conflict that avoided more hostile steps such as closing the Strait of Hormuz or direct ship-to-ship attacks. Oil prices retreated and stock prices climbed after Iran’s response avoided striking critical energy infrastructure, easing fears that the Middle East conflict would roil oil markets.

Oil prices are the key data point to watch as oil is the primary conduit through which other market prices will react. To keep a lid on oil prices, it is crucial that no disruption to oil flows through the Strait of Hormuz takes place. A super spike in oil prices above $100 per barrel would have a negative impact on the global economy and likely lead to a significant drop in global stock prices.

Oil prices are the key data point to watch as oil is the primary conduit through which other market prices will react. To keep a lid on oil prices, it is crucial that no disruption to oil flows through the Strait of Hormuz takes place.

Oil prices have largely roundtripped to levels in place before Israel launched air strikes on Iran on June 13, as investors now believe the risk is low that a major supply disruption will occur in the Middle East. Investors are, for now, betting that the delicate ceasefire will hold.

The markets were reminded of the risks associated with President Trump’s ongoing trade negotiations late last week after the President said on Truth Social that the U.S. was ending all trade talks with Canada immediately. The move was in response to Canada’s decision to impose a digital services tax on U.S. tech firms, causing stocks to pull back from their session highs. Trade threats will likely remain as issue for businesses and the stock market for the duration of President Trump’s term in office. Following the weekend, Canada rescinded its digital services tax.

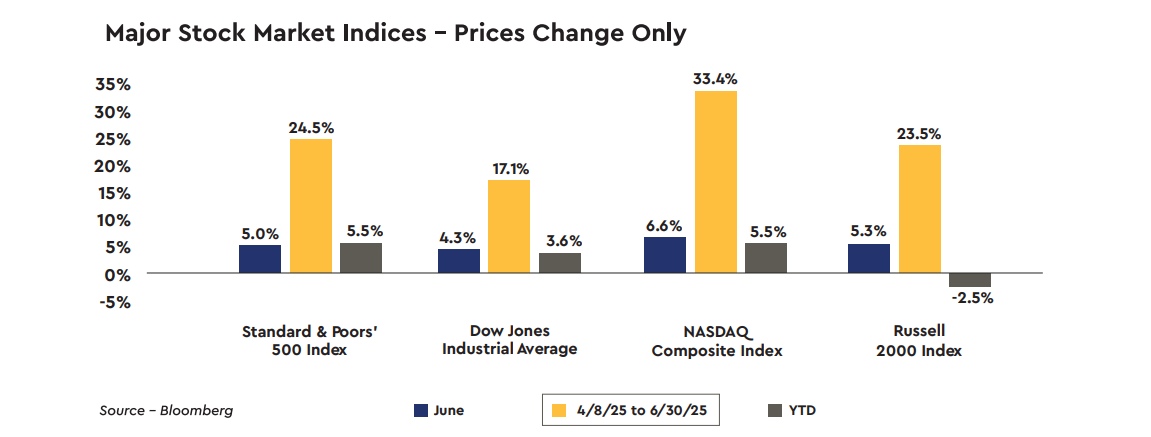

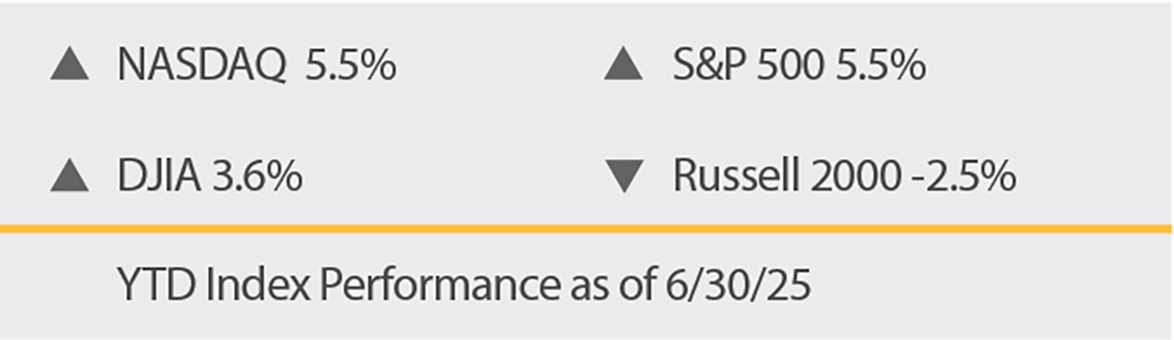

Despite the turbulent and somewhat historic events of June, the major stock market indices all posted strong gains last month, with the S&P 500 and the NASDAQ Composite reaching fresh record highs. For the month of June, the major stock market indices gained 4.3% to 6.6%. Since the recent low in stock prices on April 8 stock prices have soared with the major stock market indices higher by 17.1% to 33.4% as the Trump administration walked back the aggressive tariffs unveiled on April 2. On the year-to-date, the three large company stock measures are higher by 3.6% to 5.5% while the Russell 2000 Index of small company stocks is lower by -2.5%.

The Federal Reserve held the target range for the federal funds rate steady at the June 17-18 FOMC meeting at 4.25% to 4.50%, where it has been since December. The Committee’s new projections lowered the economy’s expected growth rate for 2025 to 1.4% from 1.7% and raised the unemployment rate to 4.5% from 4.4% and raised the outlook for core personal consumption prices to 3.1% from 2.8%. Chair Jerome Powell stated at the press conference that tariff increases are likely to push up prices and weigh on economic activity, affecting both sides of the central bank’s dual mandate.

Mr. Powell once again emphasized that the Federal Reserve needs to make sure that one-time, tariff-related price hikes do not become an inflation problem. While the Summary of Economic Projections pointed to two additional rate cuts remaining their base case for the remainder of 2025, the possibility of no rate cuts this year continues to grow. While 10 of the 19 members of the FOMC Committee penciled in two rate cuts this year, the cohort which expects that the Committee will not cut rates this year saw its ranks climb to seven, up from four in March and one in December.

This growing divide on the Committee suggests more members will not consider lowering rates without material weakness showing up in the economic data, particularly in the labor market. The prospect of tariff-related pricing pressures over the next couple of months makes it difficult for the Federal Reserve to pre-emptively cut rates. It will likely take a rise in the unemployment rate above 4.5% from the current 4.2% for the FOMC Committee to restart the rate cutting cycle.

The Federal Reserve remained on hold despite signs of a slight deterioration in the labor market, a pullback in consumer spending, and three to four months of benign inflation data. Federal Reserve officials are hesitant to lower rates without first understanding the impact on the economy of the negotiated trade deals to come. Given that the impact of trade policy will not be known for several months, the FOMC Committee is currently willing to wait for the weight of the evidence before deciding to cut rates.

Two events suggest that the Federal Reserve could shift gears on rate cuts fairly quickly, however, depending on how the economic and policy backdrop plays out. First, two Federal Reserve governors indicated in recent days that they are becoming more worried about risks of a weaker labor market rather than the risk of inflationary pressures building and could support lowering rates as soon as the next FOMC meeting at the end of July.

Second, last week Chair Powell told lawmakers at a House Financial Services Committee hearing that recent economic data would have likely justified restarting rate cuts if not for concerns that price increases from tariffs could fuel inflation and raise inflation expectations which can become self-fulfilling, particularly after four years of inflation running above the central bank’s 2% target.

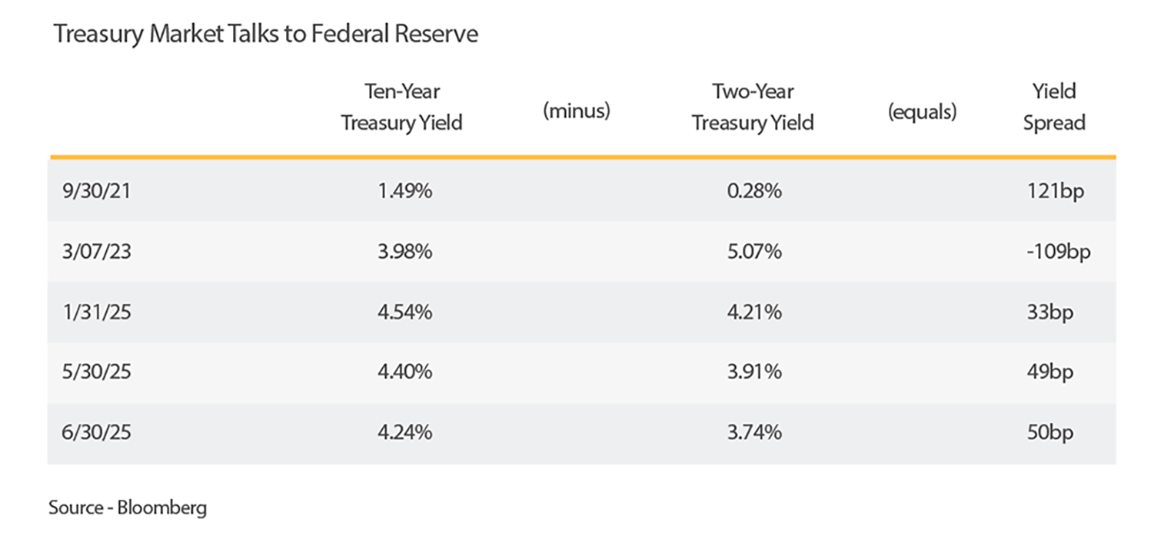

Mr. Powell stated that, “If it turns out that inflation pressures do remain contained, we will get to a place where we cut rates sooner than later, but I would not want to point to a particular meeting.” The 3.74% yield on a two-year Treasury note indicates that the markets expect the next policy move will be a rate cut, however, the timing largely depends on the extent to which tariff-related pricing pressures show up in the inflation data over the summer.

The process will provide businesses some time to anticipate and try to mitigate some of the risks associated with the ongoing derisking and further decoupling of the relationship. New supply chains and alternative sources of key components are top priorities for many businesses across the globe. Export controls will not entirely go away, but a workable situation should emerge given the incentives each country has to avoid a complete and abrupt shutdown of trade.

It is clear that the strategic direction for China and the U.S. has been set, neither country wants to be overly dependent upon the other on an array of strategic sectors. A return to a high level of engagement similar to that of the early 2000’s is not in the cards. While hopes for a trade deal are high, history says the ongoing negotiations will not be without hurdles and the likelihood of further stops and starts is quite high. This is an absolutely unique situation as the U.S. has never before faced a geopolitical adversary with which it is so economically interconnected.

Taking a step back from the narrow focus on a trade deal with China, Treasury Secretary Bessent signaled a willingness by the Trump Administration to extend the 90 day pause on the steep reciprocal tariffs beyond July 9 for the top trading partners of the U.S. that are negotiating in good faith. This is another indication that the Administration is clearly focused on de-escalating the punishing trade wars started on April 2 that placed the U.S. economy, as well as the world economy, at risk.

The markets were reminded of the risks associated with President Trump’s ongoing trade negotiations late last week after the President said on Truth Social that the U.S. was ending all trade talks with Canada immediately. The move was in response to Canada’s decision to impose a digital services tax on U.S. tech firms, causing stocks to pull back from their session highs. Trade threats will likely remain as issue for businesses and the stock market for the duration of President Trump’s term in office. Following the weekend, Canada rescinded its digital services tax.

Despite the turbulent and somewhat historic events of June, the major stock market indices all posted strong gains last month, with the S&P 500 and the NASDAQ Composite reaching fresh record highs. For the month of June, the major stock market indices gained 4.3% to 6.6%. Since the recent low in stock prices on April 8 stock prices have soared with the major stock market indices higher by 17.1% to 33.4% as the Trump administration walked back the aggressive tariffs unveiled on April 2. On the year-to-date, the three large company stock measures are higher by 3.6% to 5.5% while the Russell 2000 Index of small company stocks is lower by -2.5%.

Federal Reserve Still in No Hurry to Cut Rates

The Federal Reserve held the target range for the federal funds rate steady at the June 17-18 FOMC meeting at 4.25% to 4.50%, where it has been since December. The Committee’s new projections lowered the economy’s expected growth rate for 2025 to 1.4% from 1.7% and raised the unemployment rate to 4.5% from 4.4% and raised the outlook for core personal consumption prices to 3.1% from 2.8%. Chair Jerome Powell stated at the press conference that tariff increases are likely to push up prices and weigh on economic activity, affecting both sides of the central bank’s dual mandate. Mr. Powell once again emphasized that the Federal Reserve needs to make sure that one-time, tariff-related price hikes do not become an inflation problem. While the Summary of Economic Projections pointed to two additional rate cuts remaining their base case for the remainder of 2025, the possibility of no rate cuts this year continues to grow. While 10 of the 19 members of the FOMC Committee penciled in two rate cuts this year, the cohort which expects that the Committee will not cut rates this year saw its ranks climb to seven, up from four in March and one in December.

This growing divide on the Committee suggests more members will not consider lowering rates without material weakness showing up in the economic data, particularly in the labor market. The prospect of tariff-related pricing pressures over the next couple of months makes it difficult for the Federal Reserve to pre-emptively cut rates. It will likely take a rise in the unemployment rate above 4.5% from the current 4.2% for the FOMC Committee to restart the rate cutting cycle.

The Federal Reserve remained on hold despite signs of a slight deterioration in the labor market, a pullback in consumer spending, and three to four months of benign inflation data. Federal Reserve officials are hesitant to lower rates without first understanding the impact on the economy of the negotiated trade deals to come. Given that the impact of trade policy will not be known for several months, the FOMC Committee is currently willing to wait for the weight of the evidence before deciding to cut rates.

Two events suggest that the Federal Reserve could shift gears on rate cuts fairly quickly, however, depending on how the economic and policy backdrop plays out. First, two Federal Reserve governors indicated in recent days that they are becoming more worried about risks of a weaker labor market rather than the risk of inflationary pressures building and could support lowering rates as soon as the next FOMC meeting at the end of July.

Second, last week Chair Powell told lawmakers at a House Financial Services Committee hearing that recent economic data would have likely justified restarting rate cuts if not for concerns that price increases from tariffs could fuel inflation and raise inflation expectations which can become self-fulfilling, particularly after four years of inflation running above the central bank’s 2% target.

Mr. Powell stated that, “If it turns out that inflation pressures do remain contained, we will get to a place where we cut rates sooner than later, but I would not want to point to a particular meeting.” The 3.74% yield on a two-year Treasury note indicates that the markets expect the next policy move will be a rate cut, however, the timing largely depends on the extent to which tariff-related pricing pressures show up in the inflation data over the summer.

Think About What Could Go Right, Rather Than What Could Go Wrong

Reconvening trade talks between the U.S. and China was clearly a constructive step as the negotiators reached consensus on a framework to restore the Geneva trade war truce, but they are unlikely to completely solve the longer-term challenges facing both countries as they try to reduce their dependence upon each other. The talks will lower the risk of a rapid rupture in the relationship between the countries, however, allowing for deliberate and responsible management of the bilateral alliance.The process will provide businesses some time to anticipate and try to mitigate some of the risks associated with the ongoing derisking and further decoupling of the relationship. New supply chains and alternative sources of key components are top priorities for many businesses across the globe. Export controls will not entirely go away, but a workable situation should emerge given the incentives each country has to avoid a complete and abrupt shutdown of trade.

It is clear that the strategic direction for China and the U.S. has been set, neither country wants to be overly dependent upon the other on an array of strategic sectors. A return to a high level of engagement similar to that of the early 2000’s is not in the cards. While hopes for a trade deal are high, history says the ongoing negotiations will not be without hurdles and the likelihood of further stops and starts is quite high. This is an absolutely unique situation as the U.S. has never before faced a geopolitical adversary with which it is so economically interconnected.

Taking a step back from the narrow focus on a trade deal with China, Treasury Secretary Bessent signaled a willingness by the Trump Administration to extend the 90 day pause on the steep reciprocal tariffs beyond July 9 for the top trading partners of the U.S. that are negotiating in good faith. This is another indication that the Administration is clearly focused on de-escalating the punishing trade wars started on April 2 that placed the U.S. economy, as well as the world economy, at risk.

As long as inflation remains on a path toward the Federal Reserve’s 2% target -- leaving aside any tariff-related, one-time price bumps -- the economic cycle should continue to roll along because Federal Reserve policy should become more accommodative.

As long as inflation remains on a path toward the Federal Reserve’s 2% target -- leaving aside any tariff-related, one-time price bumps -- the economic cycle should continue to roll along because Federal Reserve policy should become more accommodative. The tax and spending bill working its way through Congress is expected to include full expensing for building a factory, equipment purchases, and research and development which should provide strong incentives for businesses to invest. Further efforts to deregulate certain sectors of the economy will also lift the economy’s growth rate.

Our view remains that the economy is in the midst of an elongated cycle, however, the disruptive tariff policies of the Trump administration are bringing about a mid-cycle slowdown. While tariffs are likely to settle out at a much higher level than at the start of the year, Corporate America is unbelievably adept at quickly adjusting to unexpected policy impacts. Continued growth in the economy will boost earnings, with earnings of U.S. multinationals receiving an extra boost from the roughly -7.1% decline in the value of the U.S. dollar over the course of 2Q 2025 through the currency translation effect, providing the necessary support for higher stock prices.

Taken with successful negotiations leading to a series of trade deals which would go a long way toward calming the fears of investors and consumers and providing businesses with some clarity on the rules of the road going forward, investors will be rewarded by thinking about what could go right, rather than about what could go wrong. While the markets still need to contend with several macroeconomic challenges, including looming tariff deadlines, the timing of the next rate cut, a tenuous ceasefire in the Middle East, and higher tariffs that will negatively impact household purchasing power, how the economy and earnings play out over the next couple quarters will determine how stock prices fare to the end of the year and into 2026.

Demand for Treasury securities was only reinforced by some good news found in recent benign inflation reports which showed that the inflation shock wave from more costly imported goods has yet to arrive on U.S. shores. A consideration is that the onetime price bumps for goods hit with tariffs leaves less money to spend on other goods and services, easing pricing pressures elsewhere.

Tariffs alter the demand for an entire array of consumer purchases because less purchasing power results from higher taxes, which tariffs ultimately are. The ultimate fallout is that the tariffs can be paid by foreign manufacturers, importers, domestic distributors, as well as by consumers. The pricing outcomes will depend upon the relative elasticities of supply and demand for each targeted good. Another consideration is that U.S. companies are applying their creativity and ingenuity to lessen the impacts of tariffs.

After initially rising following the airstrikes on Iran’s nuclear facilities, oil prices retreated as neither Israel nor the U.S. targeted Iran’s oil infrastructure, leading to no supply disruptions from the Middle East. This favorable outcome came against a backdrop of a well-supplied oil market due to recent production hikes from OPEC+. Lower energy prices have been a powerful force in the disinflationary trend over the past three years and that dynamic is likely to remain in place if no supply disruptions from the Middle East develop.

Yields on two-year and ten-year Treasury securities fell -17 and -16 basis points, respectively, during June to 3.74% and 4.24% as the positive inflation dynamics and signs of the economy’s forward momentum slowing raise the likelihood that rate cuts by the Federal Reserve could happen before year end, maybe as early as September. Given the large and growing borrowing demands of the Federal government, we are not expecting real, or inflation-adjusted, Treasury yields to fall much further in the near term unless the economy unexpectedly weakens in a material manner. Further declines in Treasury yields will largely be dependent upon inflation expectations easing further.

Our view remains that the economy is in the midst of an elongated cycle, however, the disruptive tariff policies of the Trump administration are bringing about a mid-cycle slowdown. While tariffs are likely to settle out at a much higher level than at the start of the year, Corporate America is unbelievably adept at quickly adjusting to unexpected policy impacts. Continued growth in the economy will boost earnings, with earnings of U.S. multinationals receiving an extra boost from the roughly -7.1% decline in the value of the U.S. dollar over the course of 2Q 2025 through the currency translation effect, providing the necessary support for higher stock prices.

Taken with successful negotiations leading to a series of trade deals which would go a long way toward calming the fears of investors and consumers and providing businesses with some clarity on the rules of the road going forward, investors will be rewarded by thinking about what could go right, rather than about what could go wrong. While the markets still need to contend with several macroeconomic challenges, including looming tariff deadlines, the timing of the next rate cut, a tenuous ceasefire in the Middle East, and higher tariffs that will negatively impact household purchasing power, how the economy and earnings play out over the next couple quarters will determine how stock prices fare to the end of the year and into 2026.

Fixed Income Markets

Benign Inflation and Falling Oil Prices Push Treasury Yields Lower

Yields on Treasury securities declined in a fairly persistent manner last month due to a renewed flight to safety bid and easing worries about inflation, reinforced by the decline in oil prices. The uncertainty created by both Israel and the U.S. launching airstrikes against Iran led to a fairly traditional bid for Treasury securities in a flight to the safety of U.S. government debt securities.Demand for Treasury securities was only reinforced by some good news found in recent benign inflation reports which showed that the inflation shock wave from more costly imported goods has yet to arrive on U.S. shores. A consideration is that the onetime price bumps for goods hit with tariffs leaves less money to spend on other goods and services, easing pricing pressures elsewhere.

Tariffs alter the demand for an entire array of consumer purchases because less purchasing power results from higher taxes, which tariffs ultimately are. The ultimate fallout is that the tariffs can be paid by foreign manufacturers, importers, domestic distributors, as well as by consumers. The pricing outcomes will depend upon the relative elasticities of supply and demand for each targeted good. Another consideration is that U.S. companies are applying their creativity and ingenuity to lessen the impacts of tariffs.

After initially rising following the airstrikes on Iran’s nuclear facilities, oil prices retreated as neither Israel nor the U.S. targeted Iran’s oil infrastructure, leading to no supply disruptions from the Middle East. This favorable outcome came against a backdrop of a well-supplied oil market due to recent production hikes from OPEC+. Lower energy prices have been a powerful force in the disinflationary trend over the past three years and that dynamic is likely to remain in place if no supply disruptions from the Middle East develop.

Yields on two-year and ten-year Treasury securities fell -17 and -16 basis points, respectively, during June to 3.74% and 4.24% as the positive inflation dynamics and signs of the economy’s forward momentum slowing raise the likelihood that rate cuts by the Federal Reserve could happen before year end, maybe as early as September. Given the large and growing borrowing demands of the Federal government, we are not expecting real, or inflation-adjusted, Treasury yields to fall much further in the near term unless the economy unexpectedly weakens in a material manner. Further declines in Treasury yields will largely be dependent upon inflation expectations easing further.