After a Bumpy Start to October, Stock Prices Rose Last Month

11/5/2025 - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

The economy’s growth rate should reaccelerate in 2026 following the spring/summer stall as a general fading of policy uncertainty should help provide a new steady state environment which can be relied upon and built upon and with the tax cuts and incentives in the recently passed tax legislation supporting household demand and business capital spending.

The resurgence of trade tensions between the U.S. and China, which were clearly designed to give Beijing some additional leverage in the ongoing negotiations, shows that despite months of a tariff truce and many meetings between Chinese officials and the U.S. negotiating team, relations between the world’s two largest economies remain volatile and can erupt into a crisis situation with little warning. Negotiations around major trade deals oftentimes lead to last-minute hardline positions, and China restricting access to technologically advanced materials with Washington responding by threatening 100% tariffs is a fairly predictable turn of events in the current high stakes negotiations.

Beijing knows the leverage it holds with a near monopoly on the processing of rare earth minerals. Washington’s leverage is access to the largest consumer market in the world and its sizeable lead in advanced technology, particularly semiconductors and the development of artificial intelligence. The significant economic costs for both sides of a full decoupling -- deeply disrupted supply chains, slower growth, and higher inflation -- remain the basis for a new trade agreement.

Over the weekend of October 11-12, President Trump hinted at a possible de-escalation of tariff and trade tensions with China by posting on social media “Don’t worry about China, it will all be fine!” President Trump’s effort to de-escalate comes as both nations want to lower tensions in the current trade dispute, with the Chinese Foreign Ministry stating that “China’s export controls are not export bans” and that China does not intend to harm normal trade flows.

Equity Markets

After a Bumpy Start to October, Stock Prices Rose Last Month

As investors celebrated the three-year anniversary of the bull market on October 12, common stocks ran headlong into trade war turbulence after President Trump threatened to levy a “massive increase of tariffs” on Chinese imports to counter China unveiling broad restrictions on exports of rare earth minerals. Scarcity of rare-earth metal processing, and other Chinese-dominated products like lithium and graphite, threatened to disrupt global production of mobile phones, laptops, and motor vehicles as well as militarily sensitive products such as missiles and submarines. President Trump characterized China’s actions as “extraordinarily aggressive” and suggested an expected meeting with President Xi at the upcoming APEC summit in South Korea would no longer go forward.The resurgence of trade tensions between the U.S. and China, which were clearly designed to give Beijing some additional leverage in the ongoing negotiations, shows that despite months of a tariff truce and many meetings between Chinese officials and the U.S. negotiating team, relations between the world’s two largest economies remain volatile and can erupt into a crisis situation with little warning. Negotiations around major trade deals oftentimes lead to last-minute hardline positions, and China restricting access to technologically advanced materials with Washington responding by threatening 100% tariffs is a fairly predictable turn of events in the current high stakes negotiations.

Beijing knows the leverage it holds with a near monopoly on the processing of rare earth minerals. Washington’s leverage is access to the largest consumer market in the world and its sizeable lead in advanced technology, particularly semiconductors and the development of artificial intelligence. The significant economic costs for both sides of a full decoupling -- deeply disrupted supply chains, slower growth, and higher inflation -- remain the basis for a new trade agreement.

Over the weekend of October 11-12, President Trump hinted at a possible de-escalation of tariff and trade tensions with China by posting on social media “Don’t worry about China, it will all be fine!” President Trump’s effort to de-escalate comes as both nations want to lower tensions in the current trade dispute, with the Chinese Foreign Ministry stating that “China’s export controls are not export bans” and that China does not intend to harm normal trade flows.

It is clear that the strategic direction for China and the U.S. has been set; neither country wants to be overly dependent upon the other on an array of strategic and critical goods and components.

It is clear that the strategic direction for China and the U.S. has been set; neither country wants to be overly dependent upon the other on an array of strategic and critical goods and components. A return to a high level of engagement similar to that of the early 2000’s is not in the cards. The process of reducing their dependence upon each other is not without hurdles, however, and the likelihood of additional flare-ups is quite high. This is an absolutely unique situation as the U.S. has never before faced a geopolitical adversary with which it is so economically interconnected.

The renewed trade tensions with China were followed by shares of several regional banks and alternative asset managers falling mid-month after two regional lenders disclosed issues with a handful of troubled borrowers. These problematic loan announcements followed the bankruptcies of two auto industry-related companies which raised concerns about lax lending practices, particularly in the opaque private credit market.

These credit issues do not appear to be a systemic risk to the banking system at this time, as the asset quality numbers that have been reported by large, as well as regional, banks over the past several quarters point to broad stability in credit.

Investors largely ignored the shutdown of the federal government during October as the economic impact has been negligible so far, and the negotiations were overshadowed by the artificial intelligence investments which have been a big driver of the market rally. However, pressure began to build during the month as federal workers, except for the military and law enforcement personnel, missed paychecks and the largest union of federal government workers called for an end to the shutdown.

Stock prices received a boost toward the end of the month as a positive framework of a trade deal was worked out by top Chinese and U.S. officials for President Trump and President Xi to decide on when they were scheduled to meet on October 30 at the APEC summit. Treasury Secretary Bessent said the negotiations eliminated the threat of President Trump’s 100% tariff on Chinese imports.

At the high stakes meeting in South Korea, President Trump and President Xi reached a trade truce with Beijing delaying the export controls on rare earth minerals for one year, while Washington cut the fentanyl-linked tariffs to 10% from 20%, reducing the overall tariff rate on many Chinese goods to 47% from 57%. In return, Beijing agreed to crack down on chemicals used to make fentanyl and resume purchases of U.S. soybeans, sorghum, and other agricultural products.

While the truce likely will not change the path of U.S.-China relations or raise the level of trust between the countries, it will buy time for each side to continue to de-risk from the other. China is seeking self-sufficiency in the semiconductor chip sector and needs to focus on the persistent weakness in its domestic economy. The U.S. is aggressively building alternative rare earth supply chains, which takes time and massive investments.

Additionally, the inflation report for September was cooler than expected, the Federal Reserve delivered a second consecutive rate cut at the October 28-29 FOMC meeting, credit card data pointed to solid consumer spending, and investors decided they did not want to be underexposed to common stocks during a strong quarterly earnings reporting period.

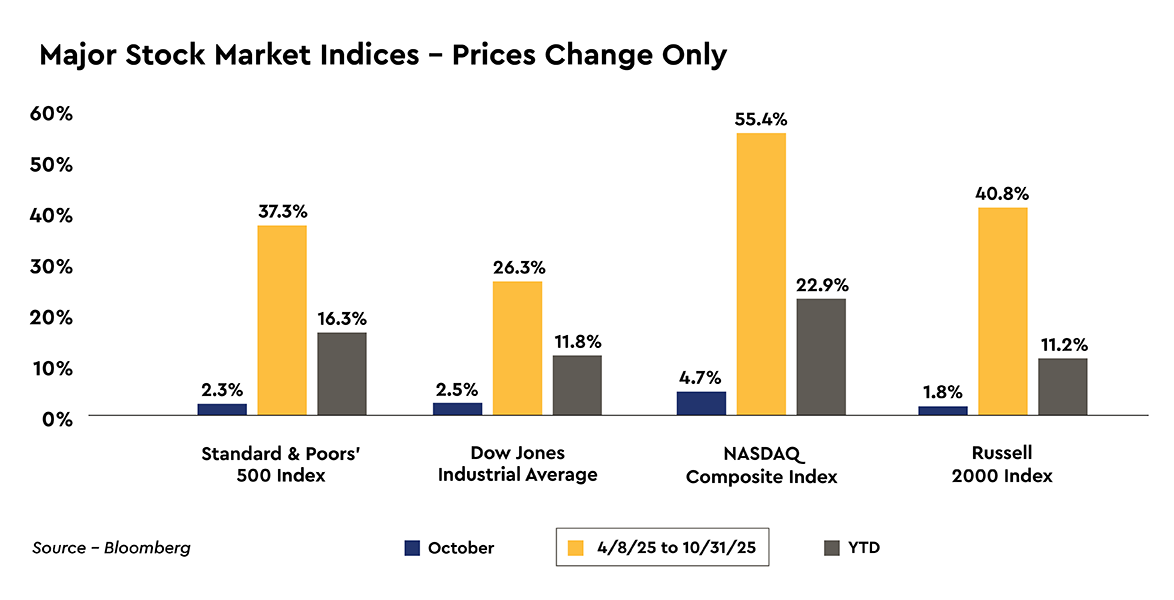

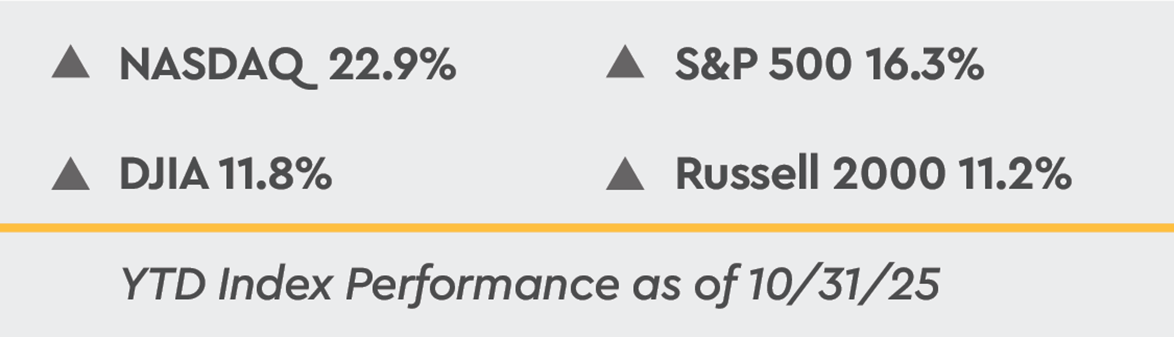

The decline in stock prices to mid-month was erased over the back half of the month with the major stock market measures gaining 1.8% to 4.7% during October. Over the first ten months of the year, the major stock market indices are higher by 11.2% to 22.9% and are higher by an impressive 26.3% to 55.4% since the recent low in stock prices on April 8.

Additionally, the Federal Reserve announced that it would stop reducing the amount of bonds it holds on its $6.6 trillion balance sheet, a campaign that has been in place since June, 2022. The central bank has reduced the size of its portfolio of Treasury and mortgage-backed securities by $2.3 trillion by allowing proceeds from maturing securities to roll off the balance sheet at a predetermined level each month. Recent signs in the overnight funding markets that banks were no longer awash in surplus cash indicated that the runoff of its bond portfolio had run its course.

While the Federal Reserve delivered the widely expected 25 basis point rate cut last week, it was not without some intrigue over the deliberations. Newly appointed Governor Stephen Miran again cast a dissenting vote, preferring that the central bank move more quickly with a 50 basis point cut. Kansas City Federal Reserve Bank President Jeffrey Schmid also dissented, but for the opposite reason because he favored no change in rates, speaking for what is an apparently growing group of Federal Reserve officials who are concerned about additional rate cuts with inflation running above the Federal Reserve’s 2% target.

Using uncharacteristically strong language, Chair Powell cautioned against assuming that another rate cut is a sure thing at the December 9-10 FOMC meeting by stating, “In the Committee’s discussions at this meeting, there were strongly differing views about how to proceed in December. A further reduction in the policy rate at the December meeting is not a foregone conclusion.” Emphasizing the point, Mr. Powell added, “Far from it.”

The renewed trade tensions with China were followed by shares of several regional banks and alternative asset managers falling mid-month after two regional lenders disclosed issues with a handful of troubled borrowers. These problematic loan announcements followed the bankruptcies of two auto industry-related companies which raised concerns about lax lending practices, particularly in the opaque private credit market.

These credit issues do not appear to be a systemic risk to the banking system at this time, as the asset quality numbers that have been reported by large, as well as regional, banks over the past several quarters point to broad stability in credit.

Investors largely ignored the shutdown of the federal government during October as the economic impact has been negligible so far, and the negotiations were overshadowed by the artificial intelligence investments which have been a big driver of the market rally. However, pressure began to build during the month as federal workers, except for the military and law enforcement personnel, missed paychecks and the largest union of federal government workers called for an end to the shutdown.

Stock prices received a boost toward the end of the month as a positive framework of a trade deal was worked out by top Chinese and U.S. officials for President Trump and President Xi to decide on when they were scheduled to meet on October 30 at the APEC summit. Treasury Secretary Bessent said the negotiations eliminated the threat of President Trump’s 100% tariff on Chinese imports.

At the high stakes meeting in South Korea, President Trump and President Xi reached a trade truce with Beijing delaying the export controls on rare earth minerals for one year, while Washington cut the fentanyl-linked tariffs to 10% from 20%, reducing the overall tariff rate on many Chinese goods to 47% from 57%. In return, Beijing agreed to crack down on chemicals used to make fentanyl and resume purchases of U.S. soybeans, sorghum, and other agricultural products.

While the truce likely will not change the path of U.S.-China relations or raise the level of trust between the countries, it will buy time for each side to continue to de-risk from the other. China is seeking self-sufficiency in the semiconductor chip sector and needs to focus on the persistent weakness in its domestic economy. The U.S. is aggressively building alternative rare earth supply chains, which takes time and massive investments.

Additionally, the inflation report for September was cooler than expected, the Federal Reserve delivered a second consecutive rate cut at the October 28-29 FOMC meeting, credit card data pointed to solid consumer spending, and investors decided they did not want to be underexposed to common stocks during a strong quarterly earnings reporting period.

The decline in stock prices to mid-month was erased over the back half of the month with the major stock market measures gaining 1.8% to 4.7% during October. Over the first ten months of the year, the major stock market indices are higher by 11.2% to 22.9% and are higher by an impressive 26.3% to 55.4% since the recent low in stock prices on April 8.

Federal Reserve Delivers Rate Cut, with a Cautious Outlook for Additional Rate Cuts

By a 10-2 vote, the Federal Reserve lowered the target range for the federal funds rate by 25 basis points to 3.75% to 4.0% at the October 28-29 FOMC meeting. This marked the second consecutive policy meeting at which the FOMC Committee cut rates, after lowering rates a full percentage point over the final three meetings of 2024. The policy statement once again referred to concerns about the labor market, saying that “downside risks to employment rose in recent months.”Additionally, the Federal Reserve announced that it would stop reducing the amount of bonds it holds on its $6.6 trillion balance sheet, a campaign that has been in place since June, 2022. The central bank has reduced the size of its portfolio of Treasury and mortgage-backed securities by $2.3 trillion by allowing proceeds from maturing securities to roll off the balance sheet at a predetermined level each month. Recent signs in the overnight funding markets that banks were no longer awash in surplus cash indicated that the runoff of its bond portfolio had run its course.

While the Federal Reserve delivered the widely expected 25 basis point rate cut last week, it was not without some intrigue over the deliberations. Newly appointed Governor Stephen Miran again cast a dissenting vote, preferring that the central bank move more quickly with a 50 basis point cut. Kansas City Federal Reserve Bank President Jeffrey Schmid also dissented, but for the opposite reason because he favored no change in rates, speaking for what is an apparently growing group of Federal Reserve officials who are concerned about additional rate cuts with inflation running above the Federal Reserve’s 2% target.

Using uncharacteristically strong language, Chair Powell cautioned against assuming that another rate cut is a sure thing at the December 9-10 FOMC meeting by stating, “In the Committee’s discussions at this meeting, there were strongly differing views about how to proceed in December. A further reduction in the policy rate at the December meeting is not a foregone conclusion.” Emphasizing the point, Mr. Powell added, “Far from it.”

Over the next six weeks Chair Powell will be navigating a Committee with what he called a “growing chorus” among the 19 Federal Reserve officials with “strongly different views” that prefer to “at least wait a cycle” before cutting rates again.

Over the next six weeks Chair Powell will be navigating a Committee with what he called a “growing chorus” among the 19 Federal Reserve officials with “strongly different views” that prefer to “at least wait a cycle” before cutting rates again. The current data blackout resulting from the shutdown of the federal government has made it more difficult for the FOMC Committee members to assess the forward momentum in the economy and the extent to which inflationary pressures could be mounting or fading.

Chair Powell acknowledged the central bank has no “risk free path.” The Federal Reserve is trying to thread the needle of making policy sufficiently accommodative to support the suddenly fragile labor market and does not want to ignore signs that changes to trade and tariff policy are squeezing spending by low- and moderate-income households and small businesses. At the same time, the central bank needs to make sure that even modest tariff-related pricing pressures do not become entrenched in higher inflation expectations and that the inflation rate does not rise at a persistent pace above the Federal Reserve’s 2% target.

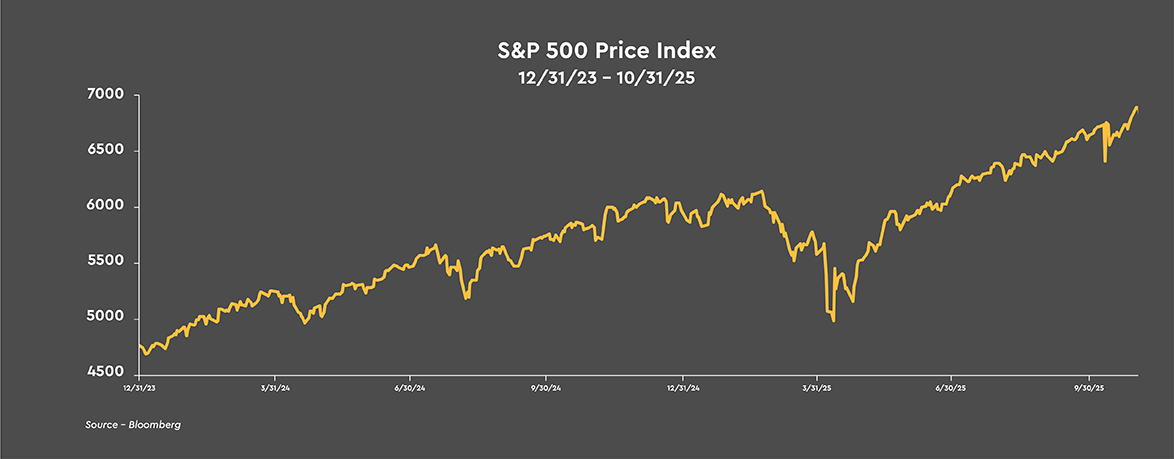

The stock market passed the three year anniversary of the start of the current bull market last month, with the S&P 500 ending October 91.2% above its low on October 12, 2022. Through the end of 2024 investors spent a little over two years pricing out significant macroeconomic risks such as fears of inflation remaining stubbornly high in a range of 3% to 4%, requiring an even more restrictive policy stance by the Federal Reserve and the economy and earnings suffering through a prolonged recessionary period.

Instead, common stock prices rose through the end of 2024 as investors priced in disinflationary influences taking hold in the economy, no recession, the start of a rate cutting cycle in late 2024, and a generally supportive backdrop for earnings which tended to surprise to the upside.

Since the beginning of 2025, however, investors once again priced in significant macroeconomic risks as they were forced to digest the scope and velocity of President Trump’s efforts to pressure U.S. trading partners and allies into meeting the administration’s demands on trade and national security issues, the strict enforcement of immigration laws, and efforts to shrink the size of the federal government and to reorient the trade norms of the global economy. The most controversial of President Trump’s policies was to significantly raise and/or impose new tariffs on trading partners.

The stress in the markets from President Trump’s policies reached a crescendo in early April following the unveiling of the “reciprocal” tariffs on April 2 which amounted to a “worst case scenario” relative to expectations, causing recession fears to mount. The stock market suffered its steepest decline since recording the significant low on October 12, 2022. From the recent record highs on February 19, the S&P 500 declined more than -20% on an intraday basis on April 8, but missed hitting bear market territory on a closing basis by dropping -18.9%.

Despite the S&P 500 gaining 37.3% since the April 8 low, the economy largely stalled over the spring and summer months as households turned very defensive fearing tariff-related higher prices and a marked softening of the labor market. Businesses pulled back on investments outside of artificial intelligence and shifted to a “slow to hire” mindset due to the rise in uncertainty and attempted to force feed some productivity gains to help absorb a portion of the tariff-related cost increases to maintain profit margins.

Chair Powell acknowledged the central bank has no “risk free path.” The Federal Reserve is trying to thread the needle of making policy sufficiently accommodative to support the suddenly fragile labor market and does not want to ignore signs that changes to trade and tariff policy are squeezing spending by low- and moderate-income households and small businesses. At the same time, the central bank needs to make sure that even modest tariff-related pricing pressures do not become entrenched in higher inflation expectations and that the inflation rate does not rise at a persistent pace above the Federal Reserve’s 2% target.

Stock Market Advance Passes Three Year Anniversary

The stock market passed the three year anniversary of the start of the current bull market last month, with the S&P 500 ending October 91.2% above its low on October 12, 2022. Through the end of 2024 investors spent a little over two years pricing out significant macroeconomic risks such as fears of inflation remaining stubbornly high in a range of 3% to 4%, requiring an even more restrictive policy stance by the Federal Reserve and the economy and earnings suffering through a prolonged recessionary period.Instead, common stock prices rose through the end of 2024 as investors priced in disinflationary influences taking hold in the economy, no recession, the start of a rate cutting cycle in late 2024, and a generally supportive backdrop for earnings which tended to surprise to the upside.

Since the beginning of 2025, however, investors once again priced in significant macroeconomic risks as they were forced to digest the scope and velocity of President Trump’s efforts to pressure U.S. trading partners and allies into meeting the administration’s demands on trade and national security issues, the strict enforcement of immigration laws, and efforts to shrink the size of the federal government and to reorient the trade norms of the global economy. The most controversial of President Trump’s policies was to significantly raise and/or impose new tariffs on trading partners.

The stress in the markets from President Trump’s policies reached a crescendo in early April following the unveiling of the “reciprocal” tariffs on April 2 which amounted to a “worst case scenario” relative to expectations, causing recession fears to mount. The stock market suffered its steepest decline since recording the significant low on October 12, 2022. From the recent record highs on February 19, the S&P 500 declined more than -20% on an intraday basis on April 8, but missed hitting bear market territory on a closing basis by dropping -18.9%.

Look for the Economy’s Growth Rate to Re-Accelerate after Spring/Summer Stall

Despite the S&P 500 gaining 37.3% since the April 8 low, the economy largely stalled over the spring and summer months as households turned very defensive fearing tariff-related higher prices and a marked softening of the labor market. Businesses pulled back on investments outside of artificial intelligence and shifted to a “slow to hire” mindset due to the rise in uncertainty and attempted to force feed some productivity gains to help absorb a portion of the tariff-related cost increases to maintain profit margins.

Despite the S&P 500 gaining 37.3% since the April 8 low, the economy largely stalled over the spring and summer months as households turned very defensive fearing tariff-related higher prices and a marked softening of the labor market.

While investors once again demonstrated a “buy the dip” mentality in April, also supporting the rise in stock prices was the sweeping tax and spending bill signed into law over the 4th of July holiday weekend, trade deals being reached with most trading partners, and the negotiation of a truce in the trade war with China. Investors also came to the conclusion that with the mid-term elections rapidly approaching and a President that kept score during his first term on the basis of economic growth and stock prices, the Trump administration had every incentive to make sure that tariffs and trade policy would ultimately be positioned and implemented in a manner that was beneficial to the economy, earnings, and common stock prices.

In the near term, it will take a continuation of the strong 3Q 2025 earnings reporting season, which started in early October, for stock prices to advance further. So far, with roughly 70% of the S&P 500 companies reporting, 3Q 2025 operating earnings are projected to have grown a strong 18.8% on a year-over-year basis, with 83% of companies reporting a positive earnings surprise. This earnings momentum is impressive in light of the uncertainty households and businesses faced last quarter and the significant cooling of the labor market.

Looking out to 2026, the outlook for the economy and common stocks starts with the ongoing momentum provided by the artificial intelligence capital expenditure super cycle that is driving massive transformative investments in semiconductors, data centers, and power systems, and which appears to still be in the early innings of its development. In addition to the momentum from artificial intelligence investments, the fundamentals look very positive. Consider that inflation should resume a slow trend toward the Federal Reserve’s 2% target as the one time tariff-related pricing pressures pass, wage growth slows, oil prices hover around $60 a barrel, and inflation-weary households continue to resist higher prices.

Additionally, the economy’s growth rate should reaccelerate following the spring/summer stall as a general fading of policy uncertainty should help provide a new steady state environment which can be relied upon and built upon and with the tax cuts and incentives in the recently passed tax legislation supporting household demand and business capital spending. Lastly, credit yield spreads remain tight, the Federal Reserve delivered two rate cuts over the past two months along with ending the runoff of its bond portfolio next month, and Treasury yields have fallen on the year bringing lower mortgage rates and other borrowing costs, such as rates on car loans. Collectively, these underlying fundamentals should provide a solid backdrop for higher common stock prices.

Given that by some measures the current level of stock prices appears to be somewhat extended, stock returns in 2026 will likely depend upon earnings growing at a sufficiently strong pace that returns will not be reliant upon an unhealthy, further expansion of price-to-earnings ratios. While a soft labor market is typically not associated with a strong economy, it can lead to higher stock prices when it cools inflationary pressures and allows the Federal Reserve to pursue a more accommodative monetary policy.

In the near term, it will take a continuation of the strong 3Q 2025 earnings reporting season, which started in early October, for stock prices to advance further. So far, with roughly 70% of the S&P 500 companies reporting, 3Q 2025 operating earnings are projected to have grown a strong 18.8% on a year-over-year basis, with 83% of companies reporting a positive earnings surprise. This earnings momentum is impressive in light of the uncertainty households and businesses faced last quarter and the significant cooling of the labor market.

Looking out to 2026, the outlook for the economy and common stocks starts with the ongoing momentum provided by the artificial intelligence capital expenditure super cycle that is driving massive transformative investments in semiconductors, data centers, and power systems, and which appears to still be in the early innings of its development. In addition to the momentum from artificial intelligence investments, the fundamentals look very positive. Consider that inflation should resume a slow trend toward the Federal Reserve’s 2% target as the one time tariff-related pricing pressures pass, wage growth slows, oil prices hover around $60 a barrel, and inflation-weary households continue to resist higher prices.

Additionally, the economy’s growth rate should reaccelerate following the spring/summer stall as a general fading of policy uncertainty should help provide a new steady state environment which can be relied upon and built upon and with the tax cuts and incentives in the recently passed tax legislation supporting household demand and business capital spending. Lastly, credit yield spreads remain tight, the Federal Reserve delivered two rate cuts over the past two months along with ending the runoff of its bond portfolio next month, and Treasury yields have fallen on the year bringing lower mortgage rates and other borrowing costs, such as rates on car loans. Collectively, these underlying fundamentals should provide a solid backdrop for higher common stock prices.

Given that by some measures the current level of stock prices appears to be somewhat extended, stock returns in 2026 will likely depend upon earnings growing at a sufficiently strong pace that returns will not be reliant upon an unhealthy, further expansion of price-to-earnings ratios. While a soft labor market is typically not associated with a strong economy, it can lead to higher stock prices when it cools inflationary pressures and allows the Federal Reserve to pursue a more accommodative monetary policy.

Treasury Market

Treasury Yields Largely Unchanged During October, but Lower on the Year

The Federal Reserve rate cuts in September and October and the sudden deterioration in the labor market have pushed Treasury yields lower on the year, particularly at the shorter end of the yield curve. The yield on the two-year Treasury note ended October at 3.61%, -64 basis points lower than at the end of 2024. For the month of October, the two-year Treasury yield fell -1 basis points as the market anticipated the rate cut by the Federal Reserve last week back in August and early September.

The Federal Reserve rate cuts in September and October and the sudden deterioration in the labor market have pushed Treasury yields lower on the year, particularly at the shorter end of the yield curve.

While the two-year Treasury yield has fallen on the year, the implied inflation expectation actually rose 21 basis points as tariff-related pricing pressures, while more moderate than feared earlier in the year, had to be priced into the yield on two-year Treasury securities. Consequently, the real yield on two-year Treasury securities has declined -85 basis points as the economy’s growth rate hit stall speed.

The yield on ten-year Treasury securities has also fallen on the year, ending October at 4.10%, -48 basis points below the 4.58% yield at the end of 2024. The inflation expectation is largely unchanged, falling -5 basis points to 2.3%, suggesting that the investors do not expect any lasting inflationary effect from the increase in tariffs. The real yield has declined -43 basis points since the end of 2024 as projected tariff revenue of about $350 billion on an annual basis moderately improves the outlook for the federal budget deficit. The recent stall in the economy has also applied some downward pressures on real yields.

During October, the ten-year Treasury yield declined -6 basis points as the shutdown of the Federal government contributed modestly to the slower pace of economic activity. The ten-year Treasury yield spent a couple days slightly below 4%, but investors again rejected the 4% yield level on the ten-year Treasury note, settling in at 4.1% at month end.

Currently, the yield on two-year Treasury notes largely reflects an expected decline in the federal funds rate over the next couple months, on the order of 25 basis points. In our view the short end of the Treasury yield curve reflects an expectation that the economy’s growth rate will pick up as 2026 unfolds and that end of the rate cutting cycle is drawing closer now that the Federal Reserve has reduced rates by a cumulative 150 basis points since September of 2024.

While it is not our base case, we acknowledge that two-year Treasury yields could drop a bit further in 2026 as the one-time price increases from tariffs roll off the inflation data, and the nation’s underlying inflation rate resumes its descent to the Federal Reserve’s 2% target. We also assume that the new chair of the Federal Reserve will attempt to take the policy rate to a neutral position, which could be closer to 3%. This could apply a little more downward pressure on two-year Treasury yields.

Where the ten-year Treasury yield settles out in coming months will likely be the result of a tug-of-war between inflation pressures falling and the economy’s growth rate picking up some steam, resulting in an environment of nominal GDP running about 4.5%. Historically, the ten-year Treasury yield gravitates toward the economy’s nominal growth rate.

As such, we do not expect the yield on the ten-year Treasury note to trade consistently below 4% over the next few quarters, unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970. We are expecting an acceleration in the economy’s growth rate to a range of 2.5% to 3% in 2026 as the economy rebounds from the 2025 stall.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.

The yield on ten-year Treasury securities has also fallen on the year, ending October at 4.10%, -48 basis points below the 4.58% yield at the end of 2024. The inflation expectation is largely unchanged, falling -5 basis points to 2.3%, suggesting that the investors do not expect any lasting inflationary effect from the increase in tariffs. The real yield has declined -43 basis points since the end of 2024 as projected tariff revenue of about $350 billion on an annual basis moderately improves the outlook for the federal budget deficit. The recent stall in the economy has also applied some downward pressures on real yields.

During October, the ten-year Treasury yield declined -6 basis points as the shutdown of the Federal government contributed modestly to the slower pace of economic activity. The ten-year Treasury yield spent a couple days slightly below 4%, but investors again rejected the 4% yield level on the ten-year Treasury note, settling in at 4.1% at month end.

Currently, the yield on two-year Treasury notes largely reflects an expected decline in the federal funds rate over the next couple months, on the order of 25 basis points. In our view the short end of the Treasury yield curve reflects an expectation that the economy’s growth rate will pick up as 2026 unfolds and that end of the rate cutting cycle is drawing closer now that the Federal Reserve has reduced rates by a cumulative 150 basis points since September of 2024.

While it is not our base case, we acknowledge that two-year Treasury yields could drop a bit further in 2026 as the one-time price increases from tariffs roll off the inflation data, and the nation’s underlying inflation rate resumes its descent to the Federal Reserve’s 2% target. We also assume that the new chair of the Federal Reserve will attempt to take the policy rate to a neutral position, which could be closer to 3%. This could apply a little more downward pressure on two-year Treasury yields.

Where the ten-year Treasury yield settles out in coming months will likely be the result of a tug-of-war between inflation pressures falling and the economy’s growth rate picking up some steam, resulting in an environment of nominal GDP running about 4.5%. Historically, the ten-year Treasury yield gravitates toward the economy’s nominal growth rate.

As such, we do not expect the yield on the ten-year Treasury note to trade consistently below 4% over the next few quarters, unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970. We are expecting an acceleration in the economy’s growth rate to a range of 2.5% to 3% in 2026 as the economy rebounds from the 2025 stall.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.