Tariff Pricing Pressures & Policy Pivot Lifts Stocks

9/3/2025 - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

Due to tariff uncertainty, our analysis suggests the economy has been mired in what we believe is a mid-cycle slowdown in the context of a longer economic cycle and expect the economy’s growth rate to accelerate as 2025 draws to a close and 2026 commences.

Investors entered August knowing that the implementation of President Trump’s broad and historically large tariff increases were going to adversely impact both sides of the Federal Reserve’s dual mandate. Namely, tariff-related pricing pressures were going to push prices of imported goods higher, while employment growth would slow as consumers turned a bit cautious, and businesses became increasingly hesitant to make additional investments in jobs and business capital spending with their expected returns on investment somewhat uncertain.

After months of uncertainty, the July employment report made it very clear that the peak level of tariff uncertainty over the April to July period corresponded with a stall in the economy’s forward momentum. While monthly jobs growth slowed to a still healthy 73,000 in July, a massive -285,000 downward revision to previously reported jobs growth in May and June suggested the labor market had not been nearly as resilient as investors had previously thought in the face of President Trump’s threats of an aggressive tariff policy. Monthly payroll employment rose an average of 35,000 from May to July, compared to a monthly average of 168,000 during 2024.

Beyond the dramatic slowing in employment, the number of people unemployed for at least six months topped 1.8 million in July, the highest level since 2017, not counting the surge in unemployment during the pandemic. The struggle to find a job highlights a weak undercurrent in a jobs market that has been jolted by tariff uncertainty and cautious businesses who are slow to hire. Stock prices pulled back on the employment report as concerns over the outlook for the economy rose.

Investor sentiment was subsequently buoyed by signs of only moderate tariff-related cost pass-throughs showing up in household furnishings and supplies and apparel in the report on consumer prices, with offsets showing up in falling energy prices, roughly flat grocery prices, and moderating shelter costs. The markets appear to be expecting only moderate, one-time pricing pressures as tariffs are fully implemented, and pre-tariff inventory rolls off.

Persistent price increases are not expected as inflation expectations have remained well anchored. Additionally, Corporate America is fast at work using its ingenuity to keep price hikes at a minimum by sourcing new suppliers and reworking supply chains, keeping a close watch on expenses, and using pricing strategies to minimize the impact of tariffs on the prices of consumer goods.

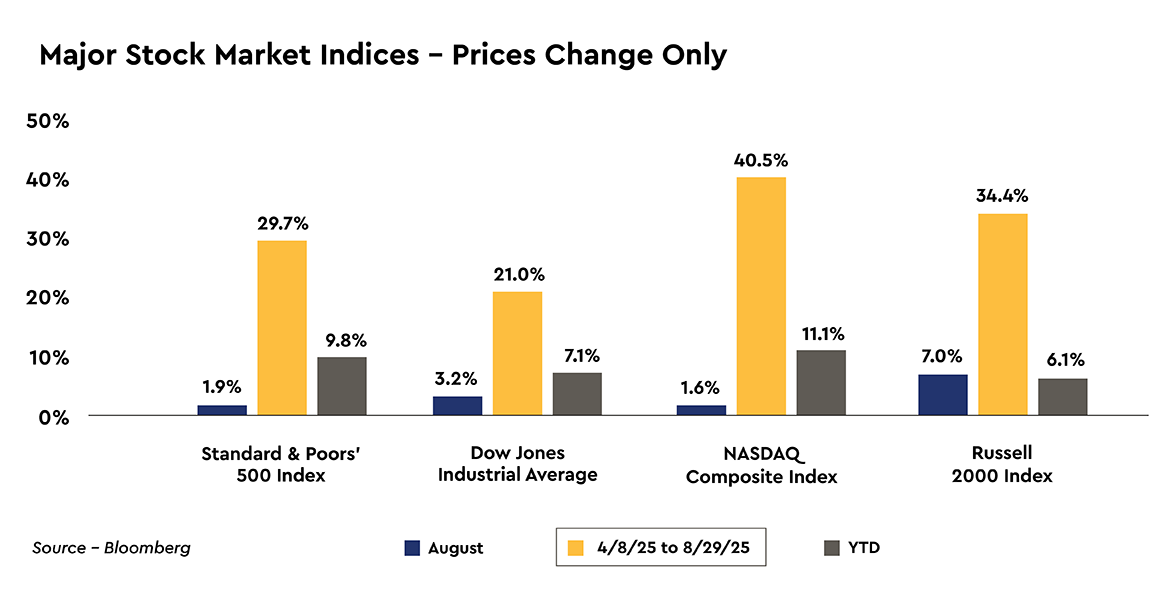

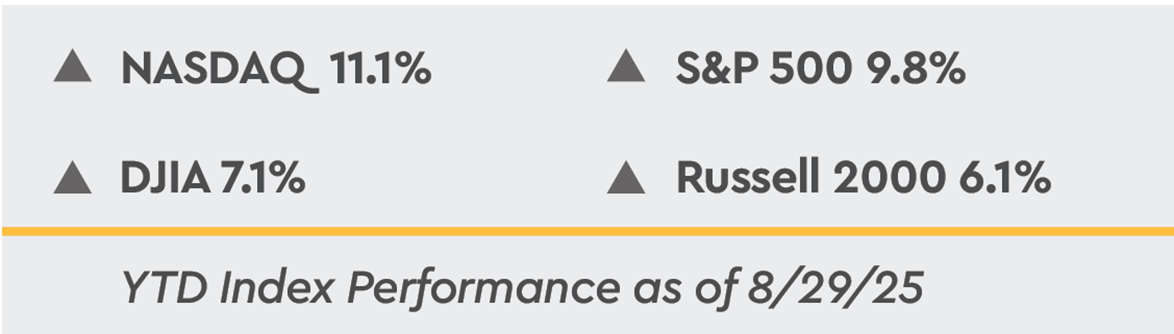

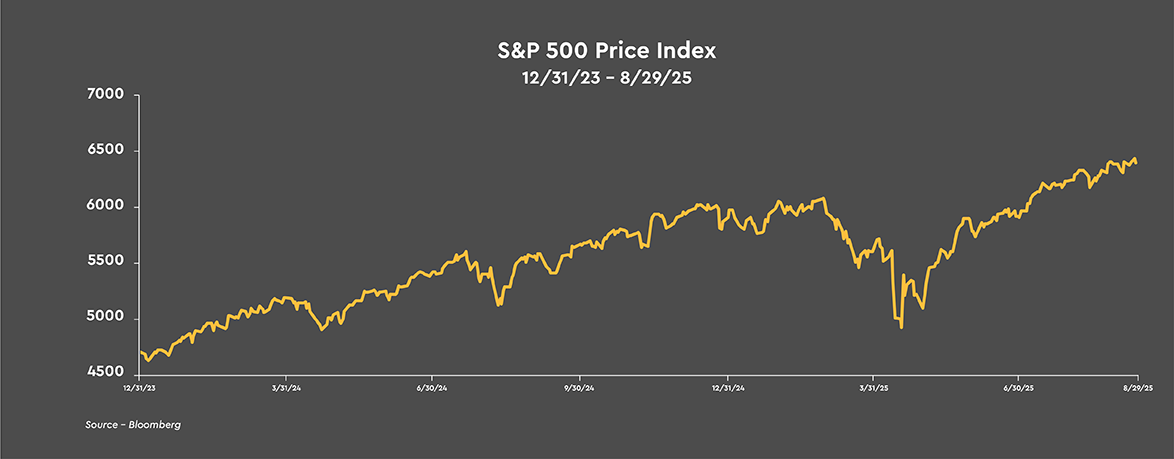

With Chair Powell opening the door to rate cuts last month and only moderate tariff-related pricing pressures, common stock prices worked their way higher during August. For the full month, the three large company stock market indices rose 1.6% to 3.2% while the Russell 2000 index of small company stocks led the way with an outsized gain of 7.0% on the expectation of rate cuts. Smaller companies tend to hold a comparatively larger portion of variable rate debt in their capital structure, debt which could become cheaper to service as rates decline. On the year-to-date, the major stock market measures are higher by 6.1% to 11.1%.

After the market close on Friday, a federal appeals court ruled that most of President Trump’s signature tariffs used to rewrite U.S. trade policy are illegal. The appeals court determined in a 7-4 ruling that only Congress has the authority to apply sweeping tariffs. The ruling injects a heavy dose of uncertainty into a core tenet of the President’s economic agenda. The judges allowed the tariffs to remain in place until October 14, however, to allow the Trump administration to appeal the ruling to the Supreme Court. Depending upon how the courts ultimately rule, some of the trade agreements announced over the past three months may need to be renegotiated, and some tariff revenue collected this year may need to be refunded.

Equity Markets

Moderate Tariff-Related Pricing Pressures and a Policy Pivot Lift Stock Prices

Investors entered August knowing that the implementation of President Trump’s broad and historically large tariff increases were going to adversely impact both sides of the Federal Reserve’s dual mandate. Namely, tariff-related pricing pressures were going to push prices of imported goods higher, while employment growth would slow as consumers turned a bit cautious, and businesses became increasingly hesitant to make additional investments in jobs and business capital spending with their expected returns on investment somewhat uncertain.

After months of uncertainty, the July employment report made it very clear that the peak level of tariff uncertainty over the April to July period corresponded with a stall in the economy’s forward momentum. While monthly jobs growth slowed to a still healthy 73,000 in July, a massive -285,000 downward revision to previously reported jobs growth in May and June suggested the labor market had not been nearly as resilient as investors had previously thought in the face of President Trump’s threats of an aggressive tariff policy. Monthly payroll employment rose an average of 35,000 from May to July, compared to a monthly average of 168,000 during 2024.

Beyond the dramatic slowing in employment, the number of people unemployed for at least six months topped 1.8 million in July, the highest level since 2017, not counting the surge in unemployment during the pandemic. The struggle to find a job highlights a weak undercurrent in a jobs market that has been jolted by tariff uncertainty and cautious businesses who are slow to hire. Stock prices pulled back on the employment report as concerns over the outlook for the economy rose.

Investor sentiment was subsequently buoyed by signs of only moderate tariff-related cost pass-throughs showing up in household furnishings and supplies and apparel in the report on consumer prices, with offsets showing up in falling energy prices, roughly flat grocery prices, and moderating shelter costs. The markets appear to be expecting only moderate, one-time pricing pressures as tariffs are fully implemented, and pre-tariff inventory rolls off.

Persistent price increases are not expected as inflation expectations have remained well anchored. Additionally, Corporate America is fast at work using its ingenuity to keep price hikes at a minimum by sourcing new suppliers and reworking supply chains, keeping a close watch on expenses, and using pricing strategies to minimize the impact of tariffs on the prices of consumer goods.

With Chair Powell opening the door to rate cuts last month and only moderate tariff-related pricing pressures, common stock prices worked their way higher during August. For the full month, the three large company stock market indices rose 1.6% to 3.2% while the Russell 2000 index of small company stocks led the way with an outsized gain of 7.0% on the expectation of rate cuts. Smaller companies tend to hold a comparatively larger portion of variable rate debt in their capital structure, debt which could become cheaper to service as rates decline. On the year-to-date, the major stock market measures are higher by 6.1% to 11.1%.

After the market close on Friday, a federal appeals court ruled that most of President Trump’s signature tariffs used to rewrite U.S. trade policy are illegal. The appeals court determined in a 7-4 ruling that only Congress has the authority to apply sweeping tariffs. The ruling injects a heavy dose of uncertainty into a core tenet of the President’s economic agenda. The judges allowed the tariffs to remain in place until October 14, however, to allow the Trump administration to appeal the ruling to the Supreme Court. Depending upon how the courts ultimately rule, some of the trade agreements announced over the past three months may need to be renegotiated, and some tariff revenue collected this year may need to be refunded.

In his widely anticipated final speech as Chair of the Federal Reserve at the annual economic symposium in Jackson Hole, Wyoming, Jerome Powell delivered a strong signal that the central bank is open to restarting rate cuts at the September 16-17 FOMC meeting.

Chair Powell Pivots in Final Jackson Hole Speech

In his widely anticipated final speech as Chair of the Federal Reserve at the annual economic symposium in Jackson Hole, Wyoming, Jerome Powell delivered a strong signal that the central bank is open to restarting rate cuts at the September 16-17 FOMC meeting. Mr. Powell highlighted that downside risks to employment are rising even as tariff-related pricing pressures are becoming more evident. Since the last rate cut in December, the FOMC committee has held rates steady, citing a healthy labor market and concerns that tariff-related pricing pressures could turn into persistent pricing pressures and raise inflation expectations, which can become self-reinforcing.While Chair Powell did not explicitly endorse a rate cut at the next policy meeting, he emphasized that “The balance of risks appears to be shifting,” which made clear that a rate cut is likely next month. Mr. Powell said, “the shifting balance of risks may warrant adjusting our policy stance,” because tariffs are unlikely to lead to sustained inflation given a weakening labor market. Following the very weak job gains in May and June at the height of the tariff uncertainty, the labor market has clearly moved front and center for the Federal Reserve as Jerome Powell highlighted its current fragility and risks to the economic outlook.

He stated that the labor market is in “a curious kind of balance that results from a marked slowing in both the supply of (changes in immigration policy) and demand for workers.” The result is an “unusual situation” in which the downside risks to employment are rising and can materialize “quickly in the form of sharply higher layoffs and rising unemployment.”

Chair Powell stressed, however, that inflation remains above the Federal Reserve’s 2% target and that tariff-related “price increases are likely to materially raise the risk of an ongoing inflation problem.” However, he stated that a “reasonable base case is that the effects will be relatively short lived -- a one-time shift in the price level.” He added that “Of course, ‘one-time’ does not mean ‘all at once.’ It will continue to take time for tariff increases to work their way through supply chains and distribution networks.”

A key determining factor in whether the Federal Reserve decides to cut rates next month will be whether or not longer-term inflation expectations “remain well anchored and consistent with our longer-run inflation objective of 2 percent.” Chair Powell emphasized that the FOMC committee will not allow tariff-related pricing pressures to become persistent by adding, “Come what may, we will not allow a one-time increase in the price level to become an ongoing inflation problem.”

President Trump and several of his advisers have placed unrelenting pressure on Chair Powell and the Federal Reserve to cut rates by repeatedly threatening to fire Mr. Powell, by trying to find “cause” for removing him by investigating cost overruns on an expensive renovation of its headquarters, and by proposing a list of successors to Mr. Powell -- who’s term as Chair ends next May -- who, on average, have argued for immediate and large rate cuts. Without mentioning President Trump by name, Chair Powell repeated his pledge that the Federal Reserve will not take political pressures into account when setting policy on interest rates and will focus only on the outlook for inflation and employment. “We will never deviate from that approach,” he said.

Chair Powell appropriately described the tension currently between the Federal Reserve’s dual mandates of full employment and low inflation, but with the clear emphasis on the downside risks for employment, his remarks made the case for a careful, cautious resumption of rate cuts. Following Chair Powell opening the door to lower interest rates in September, the markets cheered Mr. Powell’s speech with the DJIA gaining more than 800 points and notching its first record close of the year. While the DJIA played catchup to the other large company stock market indices, the gains were broad-based with stocks and bonds rallying, gold rose more than 1%, while the dollar fell.

Last week, President Trump announced he was firing Federal Reserve Governor Lisa Cook from the board of the central bank because he said there was sufficient reason to believe Governor Cook made “false statements” on one or more mortgage applications in 2021which may have enabled her to get more favorable loan terms, constituting mortgage fraud. Governor Cook challenged her termination “for cause” and said she would not resign.

Governor Cook’s attorney filed a lawsuit on her behalf challenging the President’s decision to fire her. There is little precedent for the action taken by President Trump and the right of a president to fire “for cause” and what constitutes “cause” will likely be settled in the courts. As of this writing, Governor Cook has not been charged, much less convicted, of any crime, including mortgage fraud.

Currently there is one open position on the Board of Governors following the resignation of Adriana Kugler last month and Stephen Miran, Chair of the Council of Economic Advisers, has been nominated to fill the open seat. Leaving Chair Powell aside, with two of the governors having been appointed by President Trump, adding Mr. Miran and replacing Governor Cook with a Trump appointee would result in four of the seven governors of the Federal Reserve having been appointed by President Trump.

Strong Earnings and an Improving Outlook Should Support Higher Stock Prices into 2026

With the jobs market being at the top of the list of worries about the economy at the moment, it is important to take note of the strong growth in earnings. With 96% of the S&P 500 companies reporting, 2Q 2025 operating earnings are projected to have grown a solid 10.4% on a year-over-year basis following a gain of 5.3% in the previous quarter. Corporate America is performing at a very high level as 81% of companies beat earnings estimates last quarter, an historically strong level.

Operating earnings are forecast to advance roughly 13% in the current quarter and to be 10% to 11% higher over the four quarters of 2025. The strong advance in earnings is expected to continue into 2026 with a further gain in the range of 15% to 16%. This earnings momentum is impressive in light of the tariff uncertainty businesses and households faced earlier in the year.

While earnings growth is largely dependent upon continued growth in the economy, it is also true that earnings growth bodes well for a continuation of the economic expansion because the economy tends not to slow in a material manner, or fall into recession, during a positive earnings cycle. Companies that are growing earnings are not under pressure to cut jobs, so the jobs market remains healthy, and households maintain their incomes and are not forced to cut back on spending.

As common stock prices are ultimately determined by the growth of earnings, continued growth in the economy and, in particular, a pickup in the economy’s growth rate, typically lead to further gains in stock prices. While the economy has been mired in what we believe is a mid-cycle slowdown in the context of a long economic cycle due to the tariff uncertainty President Trump has injected into the policy agenda, there are several reasons to expect the economy’s growth rate to accelerate as 2025 draws to a close and 2026 commences.

There is finally light at the end of the tariff tunnel and business and consumer confidence measures have rebounded from the trough levels reached back during the spring.

Consider that the policy uncertainty from President Trump’s tariff agenda has receded at a rapid pace since July and Treasury Secretary Bessent said the final trade deals could be wrapped up by the end of October. There is finally light at the end of the tariff tunnel and business and consumer confidence measures have rebounded from the trough levels reached back during the spring.

Combined with the Federal Reserve likely to pursue a more accommodative monetary policy in short order, energy prices lower than a year ago, a fiscal policy environment likely to settle into a new steady state that can be relied upon and built upon, the tax incentives in the new tax and spending bill for business capital spending, and ongoing efforts to lower regulations in certain sectors of the economy, the economy’s growth rate is expected to accelerate into 2026. This backdrop should set the stage for continued growth in earnings, which should provide support for higher common stock prices.

Our expectation that the economy is in the midst of an elongated economic cycle and is likely to pick up some steam in coming quarters is supported by the messaging being sent from the credit markets regarding the outlook for the economy. Once fixed income investors sense a serious downturn in the economy is approaching, they require additional yield on both investment grade and non-investment grade corporate debt compared to Treasury yields to be compensated for the greater default risk.

Currently, the yield spread on both investment grade and non-investment grade corporate debt is below the average yield spread. Namely, the current yield spread on investment grade corporate debt is 79 basis points, while the average yield spread since December 1996 is 152 basis points. Likewise, the yield spread on non-investment grade corporate debt is currently 275 basis points, far below the average yield spread since December 1996 of 542 basis points. The credit markets are not signaling that there are heightened risks of the economy falling into recession anytime soon.

Treasury Market

Treasury Yields Drop During August

Treasury yields eased during August with several factors driving Treasury yields lower. First, the stall in hiring during the spring coincided with the peak level of tariff uncertainty. While tariff-related pricing pressures have become more evident, investors took some relief in the fact that some of the most common and necessary household purchases are not experiencing outsized pricing pressures. Tariffs appear to be impacting growth more than inflation, so far. Lastly, Chair Powell’s message from Jackson Hole was that risks are more tilted to the labor market softening rather than to a persistent rise in prices from tariffs.

The largest decline in yield took place on two-year Treasury securities which fell -34 basis points to 3.63% from 3.97% at the end of July, right to the bottom of the range that has been in place since early April and the lowest yield level in three years. The likelihood that the Federal Reserve will cut rates by 25 basis points at the September 16-17 FOMC meeting and likely by a total of 50 basis points by year end pressured two-year Treasury yields lower. Two year inflation expectations rose slightly to 3.0% as investors are acknowledging the modest pricing pressures from tariffs that are showing up, and likely to continue to show up over the next few months.

At the longer end of the Treasury yield curve, the yield on the ten-year Treasury note fell -14 basis points to 4.24% from 4.38% at the end of July, to the lower end of the trading range that has been in place since mid-April once the aftershocks of the April 2 “reciprocal” tariffs worked their way through the markets. Inflation expectations out to ten years were also largely unchanged at 2.42% as investors are taking into account questions about the future independence of the Federal Reserve and the implications for longer term inflationary pressures.

At the longer end of the Treasury yield curve, the yield on the ten-year Treasury note fell -14 basis points to 4.24% from 4.38% at the end of July, to the lower end of the trading range that has been in place since mid-April once the aftershocks of the April 2 “reciprocal” tariffs worked their way through the markets. Inflation expectations out to ten years were also largely unchanged at 2.42% as investors are taking into account questions about the future independence of the Federal Reserve and the implications for longer term inflationary pressures.

The two-year Treasury yield could decline further in 2026 as the one-time price increases from tariffs roll off the inflation data and the nation’s underlying inflation rate resumes its descent to the Federal Reserve’s 2% target.

The yield on two-year Treasury notes largely reflects the expected decline in the federal funds rate to year end, on the order of 50 to 75 basis points. The two-year Treasury yield could decline further in 2026 as the one-time price increases from tariffs roll off the inflation data and the nation’s underlying inflation rate resumes its descent to the Federal Reserve’s 2% target. We also assume the Federal Reserve will pursue a somewhat less restrictive monetary policy stance with the one-time, tariff-related pricing pressures in the rear view mirror.

This outlook also assumes that President Trump’s appointee as the next Chair of the Federal Reserve brings a pragmatic approach to the policy of setting interest rates and does not attempt to engineer a policy rate lower than that supported by the economic data. We do not expect the lower end of the trading range for the ten-year Treasury note to change much over the next few quarters, unless the economy’s growth rate disappoints in large measure from the expected 2% growth rate.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve because the Federal Reserve has not yet cut rates and heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.