March 2026 - Investor Sentiment Took a Hit During February

3/4/2026 - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

Equity Markets

Investor Sentiment Took a Hit During February

February was a volatile month across several fronts. Investors opened the month by further ramping up scrutiny of artificial intelligence (AI)-related capital expenditures and dumping the stocks of enterprise software companies based on fears that AI technology could replace their current software service offerings. These AI disruption fears subsequently spilled over into other areas of the market.

For several months, investors have been concerned that the major hyperscalers (Amazon, Microsoft, and Alphabet being the top three) which provide cloud computing, networking, and internet services and run their own applications at a massive scale, plan to spend substantially more in 2026 on their AI buildout than they did in 2025.

One concern about the outsized capital expenditures is that the hyperscalers are increasingly accessing the debt markets to help finance their AI ambitions. As the AI buildout has reached levels few imagined just a couple years ago, the financial profile of some of the largest technology companies is evolving -- from cash flow rich and asset light business models with virtually no debt and extraordinary profit margins to business models that require massive investments in data centers, partially financed with debt, which squeeze cash flows and result in a capital intensive structure, but still with extraordinary profit margins.

Accordingly, investors are increasingly wanting evidence that the magnitude of the capital expenditures will be justified by future revenues, profit growth, and the likely payback period, while assessing the competitive dynamics and whether durable moats can be built in an environment where technology is evolving at breakneck speed. Additionally, the squeeze on free cash flows raises the question of the future pace of share buybacks which historically have raised earnings per share and supported stock prices for these mega cap technology companies.

Investors then turned their focus to several software-as-a service companies which sell software as a regular subscription rather than as a one-time installed product. This business model is widely used at most software companies and provides a consistent stream of income. Many of these enterprise software stocks came under selling pressure as they were seen as vulnerable to the capabilities of new AI coding tools which could lead to large companies using AI to build software for their own internal needs.

The concern that the long run disruption on Corporate America from AI might be more widespread than previously thought swept beyond enterprise software companies to other corners of the stock market. Sectors including media, legal research, data providers, financial services, payment systems, insurance and real estate brokerages, and freight logistics came under selling pressure.

While each of these industries certainly could be disrupted to some extent by AI, nobody truly knows who the long term winners and losers of this extraordinary technology will be. Given the ingenuity of U.S. companies, we are hard-pressed to embrace the doomsday scenario for wide swaths of the economy. We expect AI capabilities to empower Corporate America to improve their offerings and services by incorporating every new AI advance into their products and services, rendering them that much more useful and compelling, and likely at a lower cost.

The structure of the economy will undoubtedly be altered, however, by the AI developments and the inherent productivity improvements they will bring. The creative destruction associated with AI will deliver added pricing pressure to many industries and businesses which will increase usage, but could also drive a wave of merger and acquisition activity. The survivors will likely be the companies that pair the advantages of AI technology with their own inherent advantages of scale and expertise.

The Supreme Court struck down a significant portion of President Trump’s global tariffs on February 20 in a contentious 6 to 3 decision. The ruling stated that the President wrongly invoked the International Emergency Economic Powers Act to implement his levies on the basis that the statute does not grant the President power to levy taxes, which is singularly controlled by Congress.

President Trump responded within hours of the ruling with a 10% global tariff that he invoked under Section 122 of the Trade Act of 1974 as a work around. The statute allows for tariffs up to 15% for 150 days “to deal with large and serious U.S. balance of payment deficits.” The President raised the tariff to 15% the following day.

As of this writing, the President’s tariff regime has not ended, it was simply statutorily relocated, assuming the authority holds up in a potential court challenge on whether the U.S. currently has “large and serious… balance of payment deficits.” The balance of payments is a complete ledger of all economic transactions between the U.S. and the rest of the world.

While the U.S. current account, or trade balance, is in deficit, the capital account, which covers monetary transfers and investment transactions with the rest of the world, runs a large surplus. Under this full accounting, the current U.S. balance of payments deficit is close to zero. How long will it take for a new lawsuit to challenge the legality of the new tariff regime?

For businesses making supply-chain, pricing, and hiring decisions, the higher tariff environment has not changed in any material manner, it has been reconstituted with a 150-day expiration clock attached. Any extension of this tariff authority requires Congressional approval. The economic impact on prices and growth depends on what happens when the clock runs out of time or a legal challenge is upheld, and right now those are open questions, not settled ones.

In the meantime, separate tariffs on items such as copper, aluminum, steel, cars, trucks, lumber and auto parts are outside the scope of the Supreme Court case and remain in place. The Justices did not address whether the Treasury Department must issue refunds to companies that have been paying tariffs. There could be years of litigation to determine what happens to more than $130 billion in tariffs collected under the now invalid legal authority.

Another question is what happens to the trillions of dollars of promised investments into the U.S. that resulted from President Trump’s trade negotiations based on the ability and threat to impose onerous tariffs. The trading partners of the U.S. are currently assessing whether to stick with the trade deals negotiated last year. So far, Japan and South Korea have signaled a willingness to move forward, while European lawmakers postponed voting on approving two legal texts that are part of the trade agreement the bloc reached with the U.S. last year which would have eliminated tariffs on U.S. goods.

Lastly, geopolitical concerns hung over the market all month. While U.S. and Iranian officials continued negotiations on a deal that would curb Iran’s nuclear program, both sides have been preparing for a military confrontation, with the U.S. amassing its largest military buildup in the Middle East since Iraq was invaded in 2003, and Iran hardening its defenses and vowing to retaliate.

The United States and Israel unleased massive airstrikes against Iran early Saturday morning. The impact on the economy and the financial markets will depend upon any oil supply disruptions that result in higher oil prices, which we will be monitoring closely in coming days and weeks.

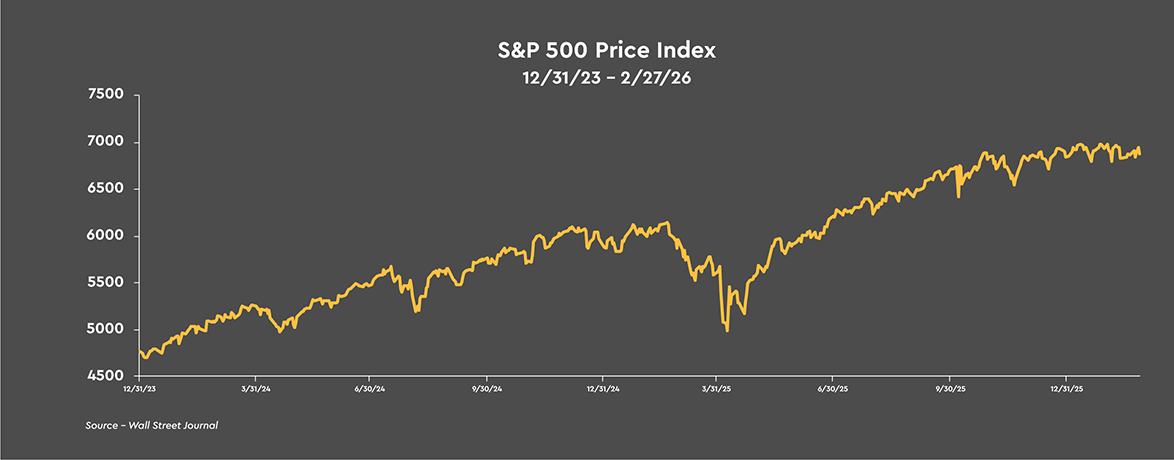

While technology stocks, particularly software stocks, and the stocks of other companies whose businesses could be disrupted by the rapid development of AI capabilities came under selling pressure last month, energy, materials, and consumer staples stocks are leading the way so far in 2026, along with industrials, as investors largely tried to stay out of the way of AI disruptions, while placing a bet on the economy’s growth rate accelerating by moving into industrials. Despite the violent rotations below the index level last month, the S&P 500 finished February only -1.4% below the record high reached on January 26.

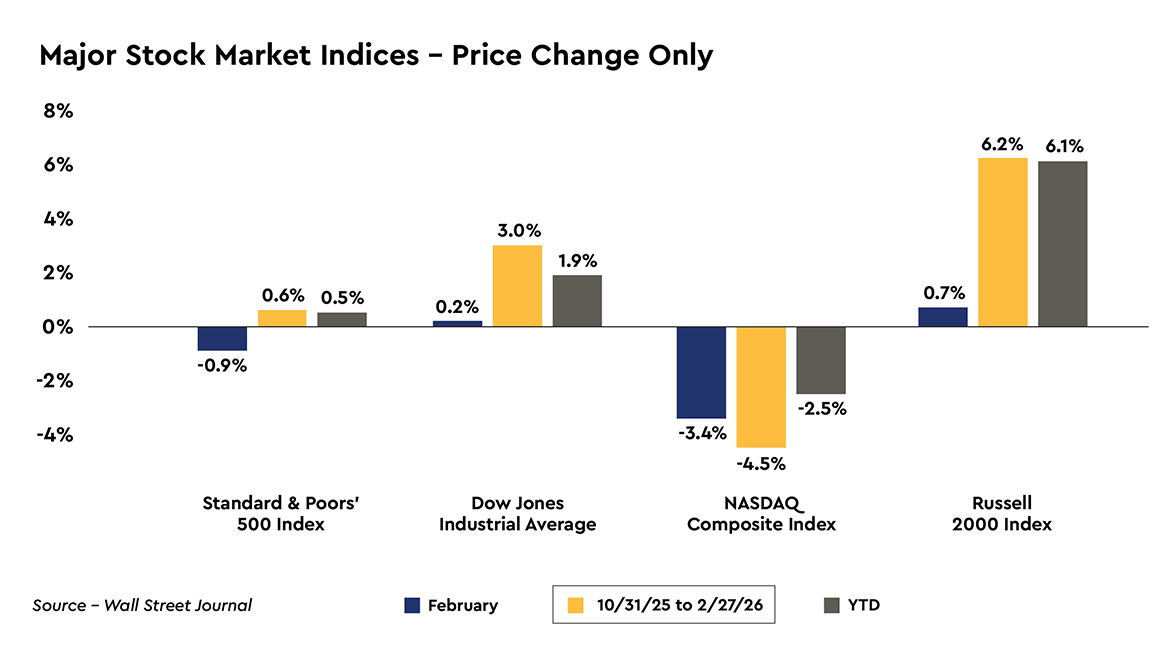

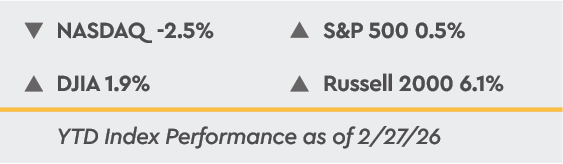

For the full month of February, the DJIA and the Russell 2000 Index of small company stocks eked out small gains of 0.2% and 0.7%, respectively, while the S&P 500 gave back -0.9% and the NASDAQ Composite posted the biggest drop at -3.4%, its worst month since March 2025. Over the first two months of 2026, only the NASDAQ Composite has posted a loss at -2.5%, while the S&P500 and the DJIA gained 0.5% and 1.9%, respectively. The Russell 2000 is leading the way so far this year, with a gain of 6.1%.

Federal Government Shutdown Holds Back 4Q 2025 Real GDP Growth

Real GDP was reported to have grown at a disappointing 1.4% annual rate in 4Q 2025, however, the federal government was shut down for almost half the quarter. Federal government expenditures contracted at a -16.6% rate, subtracting -1.2 percentage points from the real GDP figure. If the federal government had not been shut down and posted zero growth during the quarter, the economy would have grown at a 2.6% pace. Any growth in federal government outlays would have boosted the economy’s growth rate a touch faster.Consumer spending grew at a 2.4% rate, with expenditures on goods falling at a -0.1% rate and outlays for services rising at a 3.4% pace. Indications that lower and moderate income households continue to struggle were evident in real, after-tax disposable income gaining only 0.1%, after being unchanged in 3Q 2025. As such, many households needed to dip into savings to maintain spending levels, with the personal savings rate dropping to 3.6% from 4.2% in 3Q 2025 and an average of 5.1% over the first half of the year.

Business capital spending was the strongest sector of the economy, growing at a 3.7% pace, with the AI push showing up in outlays for equipment and intellectual property products rising at 3.2% and 7.4% rates, respectively. Residential construction outlays remained in the doldrums, falling at a -1.5% rate, the sixth quarterly decline in the past seven quarters. Home builders and home buyers continue to struggle with poor affordability conditions due to both high borrowing costs and home prices.

Growth last quarter and for all of 2025 was driven by the aggressive AI build out and spending by upper income households. We expect the economy’s growth rate to accelerate to a range of 2.5% to 3.0% this year compared to the 2.2% growth rate over the four quarters of 2025. Both monetary and fiscal stimulus, stronger job gains, and fading foreign trade headwinds should drive faster business capital spending and consumer spending this year, with housing outlays stabilizing and delivering a modestly higher level of activity.

Core consumer prices were higher by 2.9% on a year-over-year basis in 4Q 2025 compared to a 3.0% rise over the four quarters of 2024 despite the higher level of tariffs rolled out last year. The combination of continued growth in the economy and little change in core inflation only reinforces our view that the Federal Reserve is finished cutting interest rates through the remainder of Jerome Powell’s term as chair through May.

The key read through from the fourth quarter data is that the combination of decent growth after adjusting for the federal government shutdown and a modest gain of only 51,000 jobs during the quarter points to another solid gain in productivity, which is supportive of higher corporate profit margins and earnings.

Artificial Intelligence Fears Are Overblown, Bull Market Remains Intact

While the S&P fell a modest -0.9% last month, major changes took place under the surface with a big rotation into cyclical and value stocks and away from the narrow technology-focused, mega-cap monolith that drove stock index leadership over the past three years. Capital is not exiting risk, it is being aggressively reallocated into a much broader collection of stocks that are perceived to be undervalued and largely immune to AI disruptions. At the margin, investors are gravitating to goods producing companies rather than services companies as there is a belief that they are less likely to be disrupted by AI developments.

There is widespread fear that AI will mark the end of certain businesses and industries and that many service sector jobs will be eliminated. The history of past technological advances is that any job that requires skills that can be easily substituted by the new technology is at risk. However, we look at AI as a tool, not unlike personal computers and the internet, which will become an enhancement or augmentation of employee work efforts, enhancing the skills of employees who adapt, making them more productive and better paid.

AI will also create new businesses and jobs and will lower production costs, increasing consumers’ real incomes which can be spent on other goods and services, creating yet more jobs. At the same time, the U.S. labor market has entered a new phase where labor force growth is constrained by an aging work force and aggressive immigration policies. AI will likely help Corporate America by filling many employment gaps in the ever evolving labor force.

Data released during February suggested the economy continues to muscle ahead. Consider that solid results were reported for both services and manufacturing purchasing managers’ surveys for January. The manufacturing survey expanded for the first time in twelve months, likely reflecting the initial efforts to reshore manufacturing production to the U.S. and the business capital spending incentives contained in last year’s tax and spending bill. With the private sector adding 172,000 jobs in January, the labor market appears to be firming after registering basically no growth last year.

Despite all the attention on the potential for significant AI disruptions on a wide swath of industries and companies, we believe the bull market in common stocks is very much intact as investors need to remain focused on the big picture. Importantly, the economy is healthy, and the growth rate appears to be accelerating. Inflation is not increasing despite the higher tariffs, the labor market has stabilized and appears poised to easily outpaced last year’s modest jobs gain, and the outlook for corporate profits is for a second consecutive year of above trend earnings growth.

Since mid-2024, earnings growth has driven the current bull market rather than price-to-earnings multiple expansion, and we expect that to continue this year. Earnings growth is closing out 2025 on a strong note. So far, with roughly 96% of the S&P 500 companies reporting, 4Q 2025 operating earnings are projected to have grown 15.8% on a year-over-year basis, which would result in a 12.6% gain for full year 2025. The consensus forecast provided by FactSet is for earnings to grow more than 14% over the four quarters of 2026, which would be another significant advance.

With the significant rotations taking place in the stock market over the past couple months, valuations on mega cap technology companies have become more reasonable, falling more than the price-to-earnings ratio on the S&P 500 has dropped, although stocks still remain in the somewhat expensive category. However, with credit yield spreads very tight to Treasury securities, profit margins wide and likely to widen further with the ongoing productivity gains, and earnings growing at very rapid rates, we are not concerned with current valuation levels.

AI capabilities are becoming increasingly integrated into nearly all sectors of the economy, however, at widely divergent adoption rates depending upon the industry and company. Irrespective, the impact on productivity is unmistakable, with all levels of adoption having positive implications for productivity and profit margins. An AI-driven productivity boom will lift the economy’s non-inflationary speed limit. That would create some space for the Federal Reserve to lower the target range for the federal funds rate to a level closer to 3%, which is the outcome the federal funds futures market is currently expecting.

For the time being, healthy fundamentals are being outweighed by poor investor sentiment and mounting uncertainties over geopolitical risks, the potential for AI disruptions, and trade policy. We expect that the recent rotation into the slower growth sectors of the market will run its course in coming months, with a renewed focus on the sectors and companies demonstrating the strongest actual and potential earnings growth. As that occurs, the previous winners will likely overtake the recent, slow growth winners.

Treasury Market

Flight to Safety and Lower Inflation Expectations Push Treasury Yields Lower

Global bond yields, including U.S. Treasury yields, declined during February as a rise in geopolitical risks, lower than expected inflation and mounting risks to growth in the Eurozone, and heightened volatility in the U.S. equity resulted in a “flight to safety” among investors. In the U.S., the ten-year Treasury note yield dropped -29 basis points to 3.95% on the month, with the real yield falling -20 basis points as investors sought the perceived safety Treasury debt. The ten-year implied inflation outlook fell -9 basis points to 2.24% as longer dated inflation expectations remain well anchored.At the shorter end of the Treasury yield curve, the yield on the two-year Treasury note fell -15 basis points to 3.39%. The two year implied inflation expectation fell -11 basis points to 2.51% as near term concerns over tariffs pushing inflation higher this year have eased in a material manner compared to the 3.0% inflation expectation at the end of August.

Yields on two-year Treasury notes tend to lead the federal funds rate, and the 3.39% yield currently is 24 basis points below the 3.63% midpoint of the current target range for the federal funds rate. As such, the Treasury market is expecting one rate cut this year, while the federal funds futures market s looking for two rate cuts by the end of the year.

Where the ten-year Treasury yield settles out in coming months will likely be the result of a tug-of-war between inflation pressures falling and the economy’s growth rate picking up some steam, resulting in an environment of nominal GDP running about 4.5% to 5.0%. Historically, the ten-year Treasury yield gravitates toward the economy’s nominal growth rate.

As such, we expect the yield on the ten-year Treasury note to be under modest upward pressure over the next few quarters, unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970. We are expecting an acceleration in the economy’s growth rate to a range of 2.5% to 3% in 2026 as the economy rebounds from the 2025 stall in the labor market and responds to the fiscal and monetary stimulus in the pipeline.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.