Market Volatility, Unwelcome Oil Price Shock, and Why Staying Invested Matters

5/5/2026 - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

As we mentioned last month, investors need to keep in mind that during periods of heightened geopolitical risks markets may be volatile, but the need to remain invested is paramount, providing portfolios the opportunity to recover once the period of heightened risks is over. While we are not asserting that an end to the conflict in Iran is near or that the associated market volatility is over, the strong gains in the market last month underscored the need to maintain a steady hand with your investments when geopolitical risks rise.

Equity Market

Blockade of Iranian Ports Gives the U.S. Significant Strategic Leverage Over Iran

April opened with President Trump’s reprieve from strikes on Iran’s power plants in place until April 6. Tehran’s ability through most of the conflict to control the Strait of Hormuz became Iran’s most significant point of leverage against the U.S., its Gulf neighbors, and the global economy as it held the keys to the global energy markets. President Trump’s impatience with Iran’s refusal to reopen the strait led a major escalation of his aggressive rhetoric toward Iran. The threats and devastating bombing campaign led to a conditional two-week ceasefire during which shipping traffic was supposed to be permitted through the strait. The agreement was mediated by Pakistan and the U.S., and Iranian delegations were invited to Islamabad on April 10 to “further negotiate for a conclusive agreement to settle all disputes.”

After Vice President Vance ended 21 hours of negotiations in Pakistan on April 11 without an agreement or next diplomatic steps in sight, President Trump said the U.S. Navy would immediately begin a blockade of the Strait of Hormuz for ships using Iranian ports. Despite the cease-fire agreed to on April 7 being tied to Tehran pausing its own blockade and allowing safe passage through the strait, Iran denied passage to all non-Iranian oil and gas tankers and merchant ships. With the blockade, the U.S. flipped the Iranian strategy on its head, with the regime now suffering the consequences of its oil and petrochemical exports being blocked.

The events of last month remind us that no matter the situation or circumstance, the incentives that drive behavior and outcomes almost always come down to economics. While conventional wisdom was that the U.S. blockading the strait would leave the global energy markets in deeper trouble than before the two-week ceasefire deal was announced, investors viewed the shift from accelerating the military confrontation to economic warfare as the first step toward a constructive and lasting cessation of the conflict.

The reason is that Iran previously had an incentive to wait out the U.S. by closing the strait and keeping oil prices high and severing supply chains for liquified natural gas, refined energy products, petrochemicals, and fertilizers to sow as much economic chaos in the global markets as possible. That incentive would change if the U.S. took control of Iran’s oil revenue, but that was expected to require U.S. ground troops to control Kharg Island -- which holds little, if any, support domestically -- or destroying Iran’s oil infrastructure which would remove Iran’s oil supply for an extended period from global oil markets and make it difficult for a new regime or the defrocked remnants of the prior regime to rebuild the country and its economy.

Restricting Iran’s ability to export its crude would devastate an already battered economy. Iran now had a reason to negotiate and an incentive to restore traffic in the strait. China also had an incentive to be supportive of opening the strait as it imports roughly 11% of its oil from Iran, but nearly 50% from the Gulf states in total according to the U.S. Energy Information Administration.

According to one estimate, the U.S. blockade will cost Iran between $400 to $500 million a day, mostly in lost oil and petrochemical export revenue. Additionally, as Iran runs out of oil storage, it will be forced to shut in active wells, a costly and drastic measure that risks impairing crude production for years to come. Iran’s Hormuz vulnerability was exposed.

Under the blockade, Iran’s oil cannot be exported. Its imports cannot be delivered, including agricultural products, pharmaceuticals, machinery, transportation and technology equipment, and construction supplies needed to rebuild its battered infrastructure and economy. The blockade of Iranian ports neutralized the leverage Iran had on the global economy and increased the economic pressure on Iran to agree to a negotiated settlement with the U.S.

Rather than spiking higher, oil prices initially fell following the start of the blockade, and the S&P 500 rose to a new record high, making it clear that investors viewed the blockade of Iran’s exports as a far better alternative to putting U.S. troops in harm’s way or destroying Iran’s energy infrastructure to end Iran’s control of the strait.

While the massive military strikes on Iran failed to force them to open the Strait of Hormuz to safe passage for commercial shipping, the newfound leverage the U.S. achieved over Iran with the naval blockade of their ports inflicted such significant economic pain on the country that the battered regime declared the strait open to all commercial ships on April 17. The announcement came after a ten-day truce between Israel and Lebanon began earlier that morning after weeks of fighting.

Following the announcement from a top Iranian official that the Strait of Hormuz was “completely open,” President Trump responded that the U.S. blockade of Iranian ports would remain in place until a deal was 100% complete. This suggested that the significant economic pressure from the blockade would remain in place until Iran agreed to a list of U.S. demands involving its nuclear program, its support for terror proxies operating in the Middle East, and reopening the strait to safe passage.

In the hours following the reopening announcement, an Iranian media outlet aligned with the Islamic Revolutionary Guard Corps (IRGC), the paramilitary force tasked with defending the regime and coordinating Iran’s war efforts, began to roll back the safe passage pledge, saying Iran’s armed forces would supervise ship movements and keep the strait closed if the U.S. blockade remained in place. On April 18, the IRGC said the strait was closed. Approaching the strait “will be considered cooperation with the enemy,” the IRGC warned.

President Trump then unilaterally extended the ceasefire with Iran by two weeks a day before it was set to end, saying it was warranted due to Tehran’s “seriously fractured” government and followed a request from Pakistan’s negotiators to refrain from attacking Iran’s power plants until such time that Iran’s leaders can come up with a unified proposal. It appears Iran is dealing with a significant rift between top officials who are focused on ending the conflict and repairing Iran’s battered economy and newly empowered hardliners in the IRGC and elsewhere in the political system who are battling for control of the government.

While the conflict between Iran and the U.S. has shifted to the waters in and around the Strait of Hormuz with both sides firing on and seizing vessels they say were violating their respective restrictions on shipping, it appears the two sides may be coming closer to positions that could lead to a negotiated settlement. Consider that the U.S. has now indefinitely extended the ceasefire and announced that Israel and Lebanon agreed to extend their ceasefire by three weeks following a meeting in the White House.

Despite President Trump extending the ceasefire, a second round of negotiations between the U.S. and Iran did not take place as Iran stated that it will not return to the negotiating table until the U.S. blockade is lifted. The markets seem to be discounting a continued ceasefire until the economic and/or political pressure forces one side to push for a settlement.

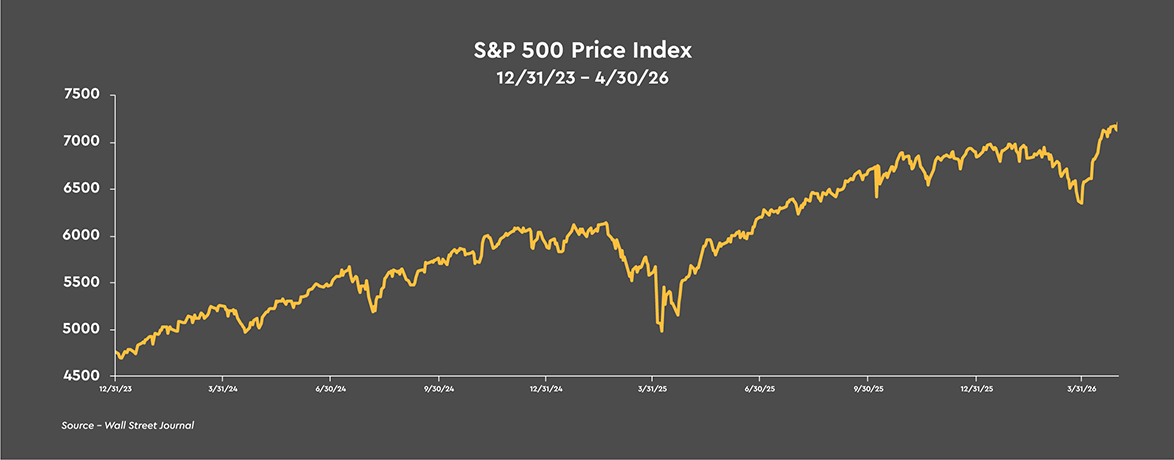

With the S&P 500 and the NASDAQ Composite reaching new all-time highs last month, the markets are expecting that the Iran conflict will remain on a path of de-escalation that will eventually lead to a workable resolution. Given the ability of the U.S. economy to weather a period of higher oil prices and the devastating chokehold the blockade is having on Iran’s economy and the potential for long-term damage to Iran’s oil wells, the markets appear to be expecting Iran to return to the negotiating table before long.

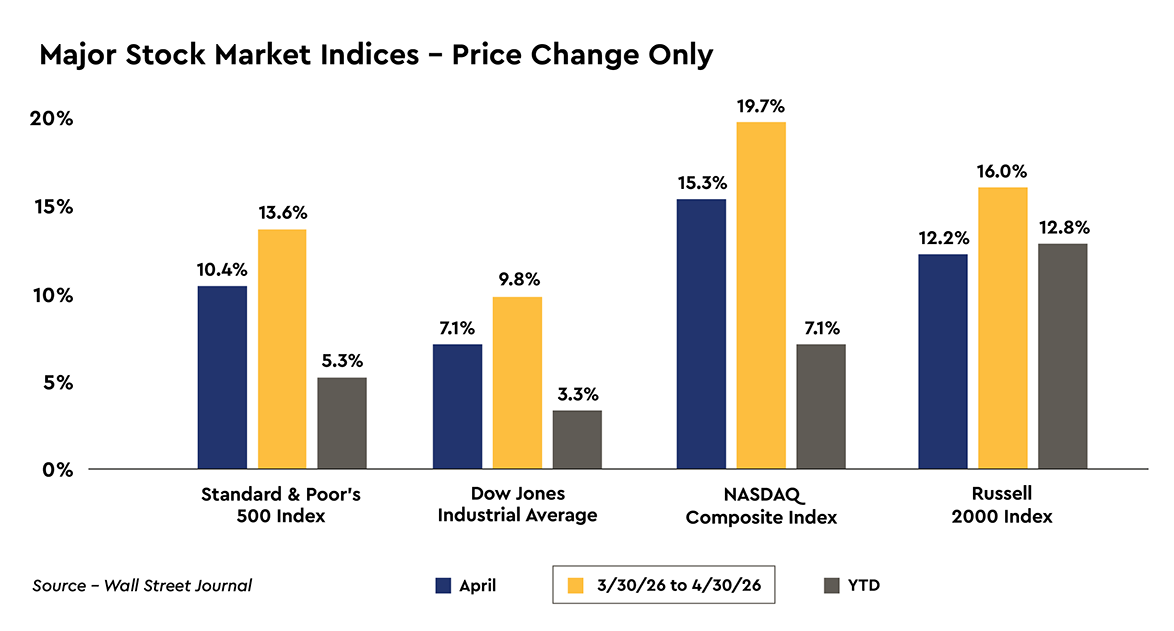

Despite oil prices ending April near two-month highs and negotiations to end the Iran war stalled, stock prices rebounded sharply last month. The NASDAQ Composite led the way with a gain of 15.3% during April as investors gravitated to the companies demonstrating the strongest actual and potential earnings growth. The other major stock market indices posted gains of 7.1% to 12.2% during April. Since the March 30 low, the major stock market measures are higher by 9.8% to 19.7%. Despite the conflict in the Middle East, the major stock market measures have gained 3.3% to 12.8% over the first four months of 2026 as strong earnings growth has outweighed geopolitical risks.

Path Cleared for Kevin Warsh to Become the Next Chair of the Federal Reserve

President Trump’s pick to be the next chair of the Federal Reserve, Kevin Warsh, was grilled at his confirmation hearing before the Senate Banking Committee on whether he would maintain the central bank’s independence from political interference. Other contentious lines of questioning centered on his reluctance to weigh in on the legality of President Trump’s attempt to fire Federal Reserve Governor Lisa Cook and the Department of Justice’s (DOJ) criminal investigation of Chair Powell, and whether the President had pressured him to commit to lower interest rates, which Mr. Trump previously said was a litmus test for any nominee.

Kevin Warsh denied that President Trump had directly asked for a commitment to lower rates and said that he had not promised the President that he would cut rates. While considering those comments, keep in mind that the chair is only one vote among twelve voting members at the meetings of the Federal Open Market Committee. Mr. Warsh presented a somewhat hawkish slant to his views on monetary policy, despite the more dovish position he held while being considered for the job by President Trump.

During the hearing, retiring Senator Thom Tillis, the swing vote on the Senate Banking Committee, repeated his intent to block Mr. Warsh’s confirmation vote before the full Senate until the DOJ dropped its criminal probe of Chair Powell’s congressional testimony last June regarding the renovation of the central bank’s office buildings. Mr. Tillis has argued that the intent of the subpoenas from the DOJ was to pressure Mr. Powell to cut interest rates or resign.

A breakthrough to move Kevin Warsh’s nomination to a confirmation vote in the Senate occurred on April 24 when the DOJ dropped its criminal investigation into Jerome Powell. The criminal probe faced an uphill battle after a federal judge quashed the subpoenas served against Chair Powell, ruling they were improper and found “essentially zero evidence” of criminal wrongdoing and said there was “abundant evidence” that the dominant purpose of the subpoenas was to pressure him to cut interest rates or resign. The DOJ referred the investigation to the Federal Reserve’s inspector general -- an independent official within government agencies tasked with detecting and preventing fraud, waste, abuse, and mismanagement -- to review the significant cost overruns in the headquarters project.

Senator Tillis said he would now support advancing Kevin Warsh’s nomination after the DOJ represented to him that the probe is “completely and fully ended” and that only a criminal referral from the inspector general would justify reopening the case. The inspector general had already been conducting an audit of the cost overruns at Chair Powell’s request since July.

With Jerome Powell’s term as chair ending on May 15 and the Senate Banking Committee approving Kevin Warsh’s nomination to become the next Federal Reserve chair on April 29, it appears Mr. Warsh will be in place by the time Mr. Powell’s leadership term ends and will be able to chair the next FOMC meeting on June 16-17.

Federal Reserve Remains on Hold, Mr. Powell to Stay on the Board of Governors

At the last FOMC meeting that Jerome Powell will chair on April 28-29, an unusually divided Committee voted 8 to 4 to hold the target range for the federal funds rate steady at 3.5% to 3.75%. Four dissenting votes is fairly dramatic, as the last time four FOMC voting members dissented was in October 1992. The policymakers assessed the policy implications of core inflation running above the Federal Reserve’s 2% target for five years and the looming leadership transition at the central bank.

Three of the dissenting votes, all presidents of regional Federal Reserve banks, backed the rate decision, but opposed the messaging in the policy statement that further rate cuts could be ahead, saying they “did not support the inclusion of an easing bias in the statement at this time.” We view the three dissenting votes by the Bank presidents as a declaration of independence that they will not be swayed by any attempts at political interference in the conduct of monetary policy. The fourth dissenting vote was cast by Trump appointee, Governor Steven Miran, as he has done since joining the central bank in September 2025, favoring a 25 basis point cut. Mr. Miran will be leaving the Board once Kevin Warsh joins the Board as chair next month.

The blockbuster news of the press conference was Chair Powell announcing that he will stay on the Board for an indefinite period -- his term as a governor ends in January 2028 -- to defend the institution from what he called unprecedented legal attacks from the Trump administration. Jerome Powell’s decision to remain on the central bank’s Board after his term as chair ends on May 15 is a departure from nearly eight decades of precedent that Federal Reserve chairs leave the Board once their term ends. The decision by Mr. Powell highlights how President Trump’s aggressive campaign to force Mr. Powell to cut interest rates is complicating the leadership handoff to Kevin Warsh.

In answering a question, Chair Powell addressed the intense criticism he has faced from President Trump, calling it “unprecedented in our 113-year history,” and said he is concerned about the impact on the institution. Mr. Powell stated that he worries that the legal attacks are putting at risk the ability of the central bank to “conduct monetary policies without taking into consideration political factors.” Chair Powell said the events of the past three months left him no choice but to remain on the Board until the threats are fully and transparently resolved. Staying on the Board will deprive President Trump of the opportunity to nominate a loyalist to the Board, but also sets the stage to see whether President Trump will follow through on his threat to fire Mr. Powell.

Getting back to monetary policy, the Federal Reserve remains in a difficult position as the oil shock creates both downward pressure on growth and upside pressure on inflation. We continue to expect no rate cuts in the near term because no matter how the data is viewed, inflation remains uncomfortably high. The minutes of the Federal Reserve’s March 17-18 FOMC meeting said “the vast majority” of officials thought progress bringing inflation down could be slower than previously expected due to lingering tariff effects on goods prices, higher oil prices not only raising energy costs, but also bleeding into transportation costs and other measures of underlying inflation, and the possibility that consumers could begin to expect further price increases.

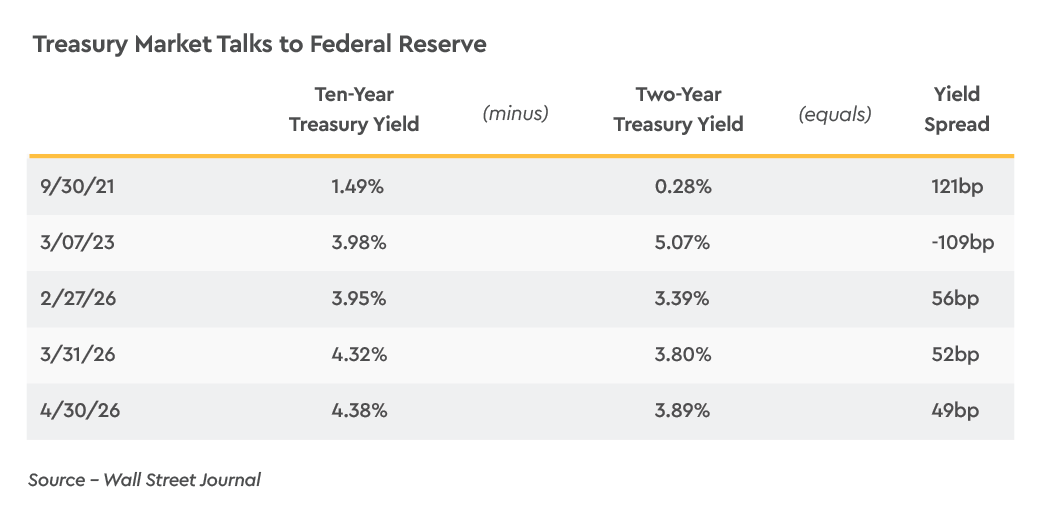

The Treasury market is also not expecting a rate cut over the next twelve months or so with the yield on the two-year Treasury note at 3.89%, higher than the 3.63% mid-point of the current 3.50% to 3.75% target range for the federal funds rate. In fact, it appears the Treasury market is pricing in roughly a 100% chance of a rate hike. The futures market for the federal funds rate is not looking for a rate cut until September 2027, with a greater probability of a rate hike rather than a rate cut during the first half of 2027.

Strong Earnings Growth Should Provide a Tailwind to Common Stock Prices

The economy remains fundamentally well-positioned with recession indicators remaining subdued and corporate earnings continuing to impress. We remain optimistic in our outlook for the economy and common stocks for 2026 with “resilience” the operative word for providing the stock market with the staying power to climb the proverbial “wall of worry.” With hindsight, it appears much of the reset for higher oil prices and supply chain disruptions was discounted to the low in stock prices on March 30.

The stock market avoided a significant capitulation or selloff because the economy continues to have solid forward momentum and oil futures are forecasting a drop in oil prices well before year-end, which has soothed both the credit and equity markets. While the markets are expecting energy prices to ease further, even in a best-case scenario where there is no additional destruction of energy infrastructure in the Gulf states, and the Strait is offering safe passage, it will take a number of months, if not years, to restore the energy market to normal.

Refineries, pipelines, ports, and other facilities must be repaired. The insurers, owners, and crews of tanker ships must be comfortable with the safety situation of moving through the Strait. There will also be a lengthy period of reserve building and global stockpiling that will impact all commodities, not just energy products, likely keeping upward pressure on prices and pressure on central banks around the globe to keep inflation and inflation expectations from rising.

It remains our view that the economy is in the midst of an elongated cycle. The tariff policy of the Trump administration during 2025 brought about a mid-cycle slowdown as households turned defensive, fearing job losses and higher prices, and businesses increasingly became hesitant to make hiring and investment decisions. That mid-cycle slowdown has extended into early 2026 as the war in Iran has raised oil prices, cutting into the real purchasing power of households that are currently dealing with higher gasoline prices, a heightened level of uncertainty, and the prospect of higher core prices as higher energy costs eventually seep into virtually every corner of the economy.

We expect that the rise in oil prices and uncertainty will likely shave the economy’s expected growth rate this year to roughly 2% compared to our prior expectation of 2.5% to 3%, with the potential for growth this year to fall below 2% the longer oil prices remain elevated. The forward momentum in the economy remains intact, however, despite some wind being taken out of its sails, due to the continued artificial intelligence buildout (think data centers), the business capital spending initiatives contained in the tax and spending bill signed into law last summer, the larger than normal tax refunds currently hitting households from the tax cuts that were retroactive to the beginning of 2025, and a more balanced regulatory regime.

April 29th’s report that economy grew at a 2.0% annualized rate in 1Q 2026, a rebound from the 0.5% pace during 4Q 2025 which was negatively impacted by the government shutdown, is consistent with our outlook for the economy. The core economy -- consumer spending, business capital spending, and residential construction outlays -- grew at a healthy 2.5% rate.

The strongest sectors of the economy were business capital spending on equipment and intellectual property products, which grew at a robust rates of 17.2% and 13.0%, respectively reflecting the aggressive data center buildout. Consumer spending grew at a 1.6% pace which should be viewed in a positive light given the jump in gasoline prices during March and particularly harsh winter weather and was led by a 2.4% gain in services outlays. On a downbeat note, the ongoing slump in housing construction showed up in an 8.0% decline, the seventh quarterly drop over the past eight quarters.

Strong earnings growth has been a dominant theme for the stock market’s resilience so far this year amid unsettling geopolitical headlines. In fact, since mid-2024, earnings growth has driven the current bull market rather than any price-to-earnings multiple expansion. Earnings estimates continue to be revised higher, suggesting that investors do not yet view the oil shock as a near-term growth issue.

With roughly 57% of the S&P 500 companies reporting, 1Q 2026 operating earnings are projected to have grown an amazing 19.6% on a year-over-year basis, compared to an expected first quarter growth rate closer to 14% at the beginning of the year. The consensus forecast provided by FactSet is for operating earnings to grow 21% over the four quarters of 2026, another significant advance.

With 84% of companies beating earnings estimates, we anticipate another year of above-trend earnings growth with the productivity and efficiency of Corporate America leading to historic profit margins. The net operating profit margin for 1Q 2026 is estimated at 16.7%, higher than the year ago profit margin of 15.9% and materially greater than the 8% to 9% profit margin of ten years ago.

While earnings growth is largely dependent upon continued growth in the economy, it is also true that earnings growth bodes well for a continuation of the economic expansion because the economy tends not to slow in a material manner, or fall into recession, during a positive earning cycle. Companies that are growing earnings are not under pressure to cut jobs, so the jobs market can remain healthy. This is a particularly important issue today given the uncertainty over how the new developments in artificial intelligence will impact the jobs market in the future.

As we mentioned last month, investors need to keep in mind that during periods of heightened geopolitical risks markets may be volatile, but the need to remain invested is paramount, providing portfolios with the opportunity to recover once the period of heightened risks is over. While we are not asserting that an end to the conflict in Iran is near or that the associated market volatility is over, the strong gains in the market last month underscored the need to maintain a steady hand with your investments when geopolitical risks rise. The initial retreat from risk assets tends not to last long and has relatively quickly been recouped so long as the economy was not already in recession or stocks in a bear market when the conflict started.

Treasury Market

Treasury Yields and Inflation Expectations Rise

Higher oil prices, the expected spread of higher energy costs across virtually all sectors of the economy over time, and higher import prices on goods from Asia and Europe that are more exposed to higher energy costs than the U.S., are expected to keep inflationary pressures uncomfortably high this year. The upward pressure on prices will only mount the longer the Strait of Hormuz remains closed.

The yield on two-year Treasury notes rose 9 basis points to 3.89% last month and is higher by 50 basis points since the United States and Israel unleashed massive airstrikes against Iran on February 28. Likewise, two-year inflation expectations rose 24 basis points during April to 3.01% and are higher by 50 basis points over the past two months. Reflecting the negative impact of higher energy costs on the economy, two-year real yields fell -15 basis points last month.

The ten-year Treasury yield rose 6 basis points to 4.38% during April and is higher by 43 basis points since the end of February. The rise in ten-year inflation expectations was more muted than on two-year Treasury securities but still rose 16 basis points to 2.45% last month and is higher by 21 basis points over the past two months.

Ten-year real yields are higher by 22 basis points over the past two months to 1.93%, largely reflecting that a larger federal budget deficit is widely expected in order to pay for the munitions used so far in the Iran War, along with an expectation that a permanently higher level of defense spending will likely be required longer term to protect the U.S. against our adversaries.

Even if inflationary pressures fall later this year if oil prices reverse a portion of their recent rise, it will be difficult for yields on longer dated Treasury yields to fall much in the future due to ever growing spending on social programs, at the same time that defense outlays and interest expense on the national debt will be under significant upward pressure.

Where the ten-year Treasury yield settles out in coming months will likely be the result of a tug-of-war between higher oil prices and other supply disruptions placing upward pressure on inflation in the near term and the economy’s growth rate muddling along at a pace of 2.0% or slightly less, resulting in an environment of nominal GDP running close to 5.0%. Historically, the ten-year Treasury yield gravitates toward the economy’s nominal growth rate over time.

As such, we do not expect the yield on the ten-year Treasury note to trade below 4% any time soon unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970. The longer energy and commodity supplies remain disrupted, the greater the near term risk to inflationary pressures, as well as, potential damage to the economy’s growth rate.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.