Slowing Jobs Market, Mild Inflation, and a Rate Cut Boost Stock Prices

10/3/2025 - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

The outlook for an acceleration in the economy’s growth rate following the mid-2025 stall remains on track. With the drag from the tariff hikes fading, energy prices lower than a year ago, ongoing efforts to lower regulations in certain sectors of the economy, and the Federal Reserve following through on additional rate cuts, the backdrop for the economy heading into 2026 should be positive.

Equity Markets

Slowing Jobs Market, Mild Inflation, and a Rate Cut Boost Stock Prices

Investors spent the first half of September focused on two key questions, “Is the data pointing to a further slowing in the jobs market or to a greater pass-through of tariff-related price hikes in the inflation data?” On the first question, the employment report for August showed that gains in the labor market slowed to a crawl following Trump administration policies that strictly enforce immigration laws and raised tariffs, which have increased uncertainty for households and businesses, weighing on the labor market. The economy added only 22,000 new jobs in August, and revisions to prior months indicated the economy lost -13,000 jobs in June, the first monthly decline since December 2020.

So far in 2025, the economy has added just 598,000 jobs, a monthly average of 75,000 compared to monthly gains of 168,000 during 2024. The weakness has been particularly pronounced since April -- the month President Trump announced his sweeping reciprocal tariffs -- with an average monthly gain of only 27,000. Businesses, which can be described as slow to hire, but also slow to fire, are attempting to force-feed productivity and efficiency gains to offset a portion of the tariff impact on prices by holding back on adding to their workforce.

The preliminary benchmark revision to the payroll data based on state unemployment insurance tax records showed -911,000 fewer jobs created for the one year period ending March 2025. The monthly average gain dropped to 70,000 from the initially reported 147,000. The report strengthened the case for the rate cut at the September FOMC meeting, as well as for the Federal Reserve to cut rates again before year end.

Our key takeaway from the revised jobs data is that the economy grew 2.0% year-over-year through 1Q 2025 with fewer workers employed than previously thought. This points to stronger productivity than previously reported, which is the main driver of higher standards of living and a key driver of earnings growth. Stronger productivity supports higher profit margins and clearly contributed to the 9.7% year-over-year gain in earnings for the S&P 500 companies in 2Q 2025 and the continued strong outlook for earnings through year end.

On the inflation front, the producer price index surprisingly fell -0.1% in August and is higher by 2.6% year-over-year. Services prices posted a drop of -0.2% while goods prices increased, but just 0.1%. With inflation barely having a heartbeat at the producer level during August, the tariff effect is applying only modest upward pressure on prices so far. While the consumer price index rose 0.4% in August, there was scant evidence of tariff-related cost pass-throughs as the largest increases were found in energy (0.7%), airfares (5.9%), shelter (0.4%), and lodging (2.3%). Core consumer prices are higher by 3.1% year-over-year, unchanged from July, indicating that pricing pressures are not spreading.

Our view remains that households are adjusting their spending patterns in response to the cumulative impact of price increases since 2021 and now to the modest grind higher in goods prices as pre-tariff inventories are depleted. The inflation data over the past two to three months implies that not only will the tariff-related price increases be a one-time event, they likely will be smaller than expected despite the extent to which tariffs have been increased. With market-based inflation expectations still looking anchored, we are not expecting a persistent rise in inflationary pressures related to the tariffs.

Inflation weary consumers -- inflation-adjusted median household income in 2024 was largely unchanged from 2019 before the pandemic hit,

and inflation surged -- are forcing foreign manufacturers/exporters and domestic retailers/importers to collectively absorb the largest portion of the tariffs so far.

and inflation surged -- are forcing foreign manufacturers/exporters and domestic retailers/importers to collectively absorb the largest portion of the tariffs so far.

Consumers appear to be paying the smallest portion of the tariffs so far, as the flow-through to consumer prices remains contained. Inflation weary consumers -- inflation-adjusted median household income in 2024 was largely unchanged from 2019 before the pandemic hit, and inflation surged -- are forcing foreign manufacturers/exporters and domestic retailers/importers to collectively absorb the largest portion of the tariffs so far. “Forced” productivity gains arising from U.S. companies being reluctant to hire since April are allowing domestic retailers to absorb a portion of the tariffs without damaging their profit margins.

Better than expected retail sales in August, despite a cooling labor market, provided support to common stocks going into the September FOMC meeting where it was widely expected that the Federal Reserve would cut rates. While common stock prices have steadily risen since the reciprocal tariff lows on April 8, the rally in common stocks picked up steam following the weak jobs report released on August 1 which foreshadowed the September rate cut.

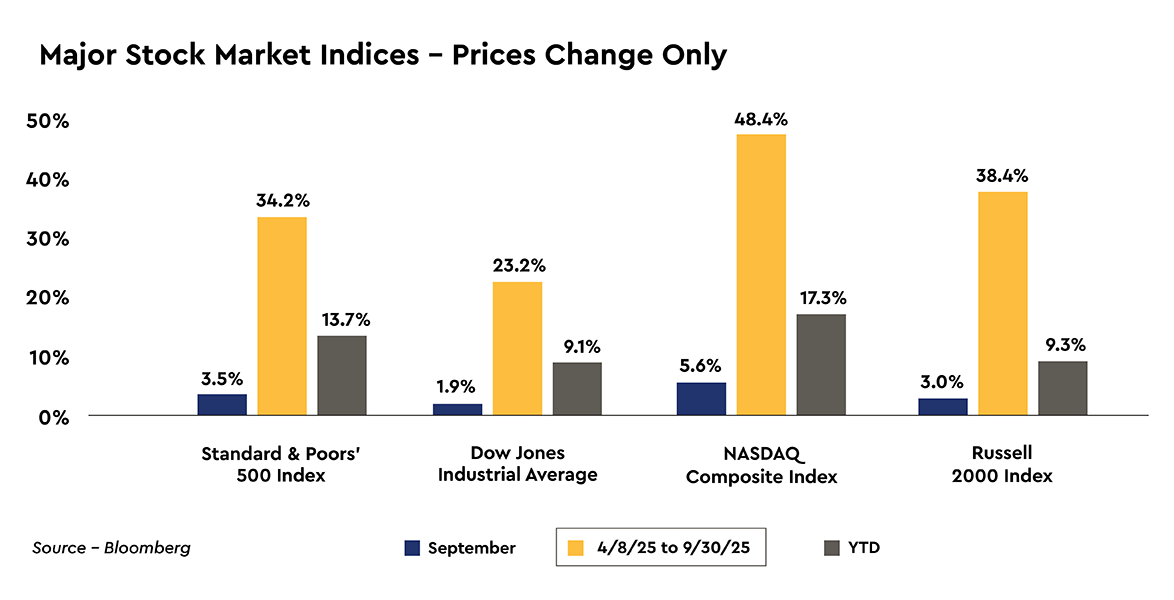

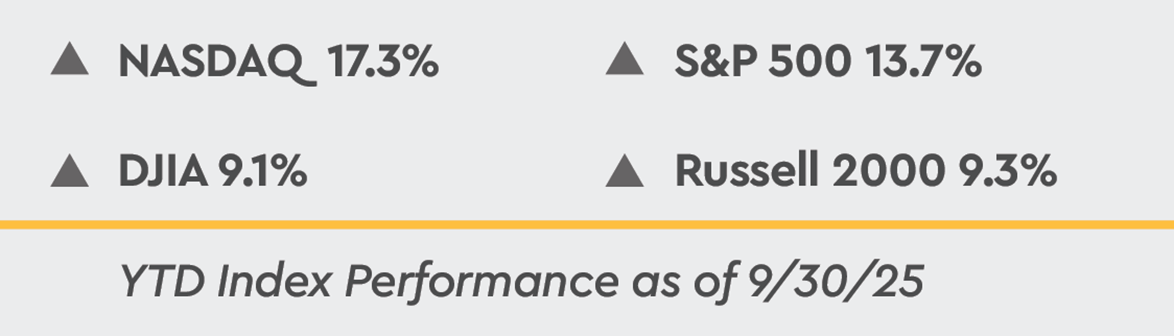

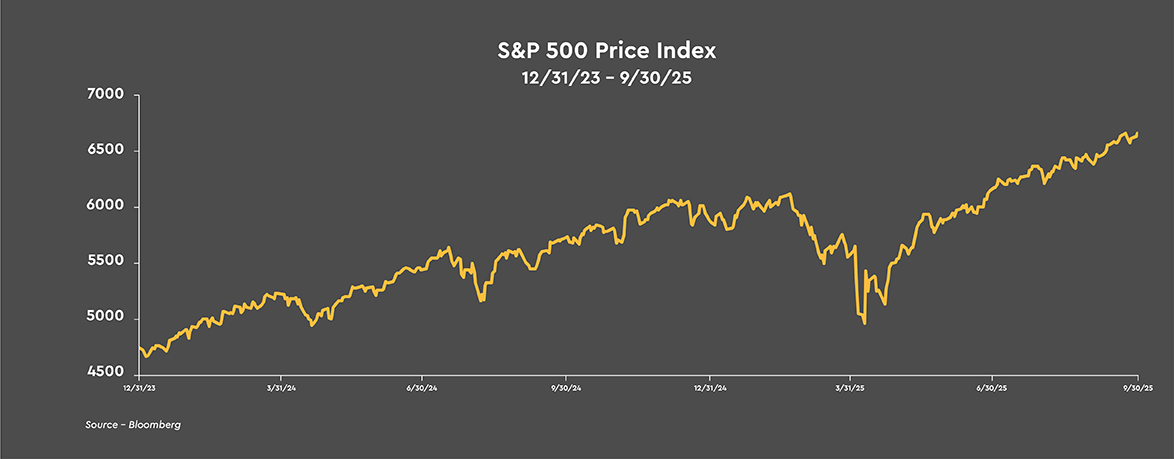

Following the rate cut last month, stock prices largely moved sideways over the back half of the month as investors digested the run up to the rate cut and the modest back up in Treasury yields to month end. Stock prices rose across the board during September, with the major stock market indices higher by 1.9% to 5.6%. Over the first nine months of the year the major stock market measures are higher by 9.1% to 17.3% and are higher by an impressive 23.2% to 48.4% since the recent low in stock prices on April 8.

The Federal Reserve lowered the target range for the federal funds rate by 25 basis points to 4.0% to 4.25% at the September 16-17 FOMC meeting. The Committee followed through with a rate cut after Chair Jerome Powell indicated in his speech at the annual economic symposium of the Federal Reserve in August that a rate cut was more likely than not at the meeting. The rate cut was the first of 2025 as the employment picture has deteriorated in a material manner since the last FOMC meeting in late July.

At the July 29-30 FOMC meeting, payroll gains were reported to have averaged 150,000 a month over the three months ending in June. Since then, that monthly payroll gain to the end of June has been revised substantially lower to 55,000, while monthly payroll gains have declined further to only 29,000 for the three months ending in August. Chair Powell stated at the press conference that the decline in the number of people gaining employment has “certainly gotten everyone’s attention” and that the rate cut was justified “in light of the shift in the balance of risks” to maximum employment and price stability.

While the Summary of Economic Projections indicated that the median committee member is looking for two additional rate cuts this year, the individual projections indicate that the October and December deliberations could be more contentious as there was a wide dispersion of rate forecasts. Seven of the 19 meeting participants are expecting no further rate cuts this year, and two penciled in only one more cut.

Federal Reserve officials are navigating an economy that has been hit with much higher tariffs and a sharp curb on immigration, but also strong incentives for business capital spending and retroactive personal income tax cuts for certain low and moderate income households that will result in higher income tax refunds than typical in early 2026. These major policy shifts have made the economy much more difficult to read.

Better than expected retail sales in August, despite a cooling labor market, provided support to common stocks going into the September FOMC meeting where it was widely expected that the Federal Reserve would cut rates. While common stock prices have steadily risen since the reciprocal tariff lows on April 8, the rally in common stocks picked up steam following the weak jobs report released on August 1 which foreshadowed the September rate cut.

Following the rate cut last month, stock prices largely moved sideways over the back half of the month as investors digested the run up to the rate cut and the modest back up in Treasury yields to month end. Stock prices rose across the board during September, with the major stock market indices higher by 1.9% to 5.6%. Over the first nine months of the year the major stock market measures are higher by 9.1% to 17.3% and are higher by an impressive 23.2% to 48.4% since the recent low in stock prices on April 8.

Policy Pivot Delivers First Rate Cut of 2025

The Federal Reserve lowered the target range for the federal funds rate by 25 basis points to 4.0% to 4.25% at the September 16-17 FOMC meeting. The Committee followed through with a rate cut after Chair Jerome Powell indicated in his speech at the annual economic symposium of the Federal Reserve in August that a rate cut was more likely than not at the meeting. The rate cut was the first of 2025 as the employment picture has deteriorated in a material manner since the last FOMC meeting in late July.At the July 29-30 FOMC meeting, payroll gains were reported to have averaged 150,000 a month over the three months ending in June. Since then, that monthly payroll gain to the end of June has been revised substantially lower to 55,000, while monthly payroll gains have declined further to only 29,000 for the three months ending in August. Chair Powell stated at the press conference that the decline in the number of people gaining employment has “certainly gotten everyone’s attention” and that the rate cut was justified “in light of the shift in the balance of risks” to maximum employment and price stability.

While the Summary of Economic Projections indicated that the median committee member is looking for two additional rate cuts this year, the individual projections indicate that the October and December deliberations could be more contentious as there was a wide dispersion of rate forecasts. Seven of the 19 meeting participants are expecting no further rate cuts this year, and two penciled in only one more cut.

Federal Reserve officials are navigating an economy that has been hit with much higher tariffs and a sharp curb on immigration, but also strong incentives for business capital spending and retroactive personal income tax cuts for certain low and moderate income households that will result in higher income tax refunds than typical in early 2026. These major policy shifts have made the economy much more difficult to read.

Currently, the FOMC is primarily reacting to employment data that indicates the jobs market was somewhat weaker heading into the April reciprocal tariff announcements than previously thought and has taken another shift lower since April as the tariff hikes have raised the level of uncertainty for households and businesses.

Currently, the FOMC is primarily reacting to employment data that indicates the jobs market was somewhat weaker heading into the April reciprocal tariff announcements than previously thought and has taken another shift lower since April as the tariff hikes have raised the level of uncertainty for households and businesses. In response, the Committee and Chair Powell are signaling a cautious shift from a moderately restrictive monetary policy focused on lowering inflationary pressures to a neutral policy that attempts to balance inflation concerns with mounting worries about the deterioration in the jobs market.

In a very unusual twist, the composition of voting members at the September FOMC meeting was not determined until the day before the two day meeting began. Early in the month, a federal judge blocked President Trump from removing Governor Lisa Cook from the Board of Governors while a lawsuit challenging her termination for alleged misrepresentations in her personal finances plays out in the courts. “The public interest in Federal Reserve independence weighs in favor of Cook’s reinstatement,” the U.S. District Court Judge wrote in granting Cook an injunction that temporarily barred her termination.

Justice Department attorneys submitted an emergency request to pause the lower court ruling, but a federal appeals court ruled the day before the September FOMC meeting started that the President could not fire Governor Cook before the central bank’s policy committee meeting convened. The appeals court said the Administration had “not satisfied the stringent requirements for a stay pending appeal,” allowing Cook to participate in the pivotal two day meeting on whether to lower interest rates.

President Trump’s unprecedented effort to remove a member of the Board of Governors “for cause” follows months of the President badgering the central bank to cut interest rates, fueling concerns about inflation and the longer term risks to the independence of the Federal Reserve. The Supreme Court is expected to have the final say in the case. The attempt to fire Governor Cook was not the only source of political drama heading into the September meeting.

President Trump nominated Stephen Miran, the Chair of the White House’s Council of Economic Advisors, to fill the remaining term of former Federal Reserve Governor Adriana Kugler who resigned August 8. Her unexpired term ends in January 2026. Mr. Miran was confirmed by the Senate to serve on the Board of Governors just hours before the Federal Reserve’s two day monetary policy meeting began. It is somewhat extraordinary that Mr. Miran did not resign from his position at the White House while he serves on the Board of Governors, instead taking an unpaid leave with the intention to return to his White House position when his term ends.

The Federal Reserve, by law and tradition, is an independent and nonpartisan federal agency established in 1913 to provide a safe, flexible, and stable monetary and financial system. It is unprecedented that now, for the first time in its history, a Federal Reserve Governor is also technically an employee of the President. Mr. Miran was the lone dissenter to the 25 basis point rate cut, favoring a larger half point cut, and a federal funds rate below 3% by the end of the year. Mr. Miran’s appointment represents another step in President Trump’s ongoing bid to bend the historically independent Federal Reserve to his will.

While Jerome Powell and the Federal Reserve have been under a largely unprecedented attack from the Trump administration over the past eight months, we expect the independence of the Federal Reserve will be maintained as Treasury Secretary Bessent is likely to guide President Trump toward nominating a pragmatist who thinks monetary policy is currently too restrictive, but clearly supports the independence of the Federal Reserve as a fundamental underpinning for a credible central bank.

In a very unusual twist, the composition of voting members at the September FOMC meeting was not determined until the day before the two day meeting began. Early in the month, a federal judge blocked President Trump from removing Governor Lisa Cook from the Board of Governors while a lawsuit challenging her termination for alleged misrepresentations in her personal finances plays out in the courts. “The public interest in Federal Reserve independence weighs in favor of Cook’s reinstatement,” the U.S. District Court Judge wrote in granting Cook an injunction that temporarily barred her termination.

Justice Department attorneys submitted an emergency request to pause the lower court ruling, but a federal appeals court ruled the day before the September FOMC meeting started that the President could not fire Governor Cook before the central bank’s policy committee meeting convened. The appeals court said the Administration had “not satisfied the stringent requirements for a stay pending appeal,” allowing Cook to participate in the pivotal two day meeting on whether to lower interest rates.

President Trump’s unprecedented effort to remove a member of the Board of Governors “for cause” follows months of the President badgering the central bank to cut interest rates, fueling concerns about inflation and the longer term risks to the independence of the Federal Reserve. The Supreme Court is expected to have the final say in the case. The attempt to fire Governor Cook was not the only source of political drama heading into the September meeting.

President Trump nominated Stephen Miran, the Chair of the White House’s Council of Economic Advisors, to fill the remaining term of former Federal Reserve Governor Adriana Kugler who resigned August 8. Her unexpired term ends in January 2026. Mr. Miran was confirmed by the Senate to serve on the Board of Governors just hours before the Federal Reserve’s two day monetary policy meeting began. It is somewhat extraordinary that Mr. Miran did not resign from his position at the White House while he serves on the Board of Governors, instead taking an unpaid leave with the intention to return to his White House position when his term ends.

The Federal Reserve, by law and tradition, is an independent and nonpartisan federal agency established in 1913 to provide a safe, flexible, and stable monetary and financial system. It is unprecedented that now, for the first time in its history, a Federal Reserve Governor is also technically an employee of the President. Mr. Miran was the lone dissenter to the 25 basis point rate cut, favoring a larger half point cut, and a federal funds rate below 3% by the end of the year. Mr. Miran’s appointment represents another step in President Trump’s ongoing bid to bend the historically independent Federal Reserve to his will.

While Jerome Powell and the Federal Reserve have been under a largely unprecedented attack from the Trump administration over the past eight months, we expect the independence of the Federal Reserve will be maintained as Treasury Secretary Bessent is likely to guide President Trump toward nominating a pragmatist who thinks monetary policy is currently too restrictive, but clearly supports the independence of the Federal Reserve as a fundamental underpinning for a credible central bank.

The next chair of the Federal Reserve...will likely hold to the position that the bond market is ultimately in control of Treasury yields and most borrowing costs and must view the next chair of the Federal Reserve as a credible central banker who will pursue both sides of the dual mandate: maximum employment and price stability.

The next chair of the Federal Reserve, similar to Secretary Bessent, will likely hold to the position that the bond market is ultimately in control of Treasury yields and most borrowing costs and must view the next chair of the Federal Reserve as a credible central banker who will pursue both sides of the dual mandate: maximum employment and price stability. Any acknowledgement of taking the cost of funding the national debt into consideration when making monetary policy decisions would be viewed very negatively by the markets, and rightly so in our view.

It appears to us that the economy is beginning to emerge from a tariff-related stall and a series of forced adjustments since April. How long the process will take is unclear. Continued growth in earnings is important as companies that are growing earnings are not under pressure to cut jobs, allowing households to maintain their incomes and spending levels. While close to 150,000 federal government workers are set to roll off government payrolls this month, lower Treasury yields and the Federal Reserve starting a rate cutting cycle should support the economy into year end.

The outlook for an acceleration in the economy’s growth rate following the mid-2025 stall remains on track. With the drag from the tariff hikes fading, energy prices lower than a year ago, ongoing efforts to lower regulations in certain sectors of the economy, and the Federal Reserve following through on additional rate cuts, the backdrop for the economy heading into 2026 should be positive.

Business capital spending incentives contained in the tax and spending bill signed into law last summer and a larger than normal level of income tax refunds from tax cuts retroactive to the beginning of 2025 will also provide the economy with a boost in early 2026, setting the stage for continued growth in earnings which should provide support for higher common stock prices.

Of course, just a general fading of policy uncertainty going forward should help provide a new steady state policy environment which can be relied upon and built upon, which would be broadly supportive of improved business confidence. Indications currently are that tariff-related pricing pressures are likely to be contained and market-based inflation expectations are consistent with inflation returning to the Federal Reserve’s 2% target over the next two years. Lastly, we remain optimistic about the long run given the inherent dynamics of the U.S. capitalistic economy to drive higher levels of earnings through innovation, creativity, self-interest to grow, and the desire for higher standards of living.

As September drew to a close, the nation faced another shutdown of the federal government -- 14 since 1981, many lasting only a day or two -- as lawmakers remained far apart on negotiations to pass annual funding appropriations for government agencies and programs. Under a shutdown, approximately 40% of federal employees (about 750,000) deemed “non-essential” would be furloughed and no federal employees would be paid until after funding is restored. In addition to permanently extending Affordable Care Act funding set to expire at the end of the year, Democrats are demanding to reinstate the cuts and changes to Medicaid that were part of the sweeping tax and spending bill signed into law last summer.

It is important to distinguish a federal government shutdown from an extension of the national debt ceiling which could result in a default on interest payments on U.S. Treasury securities if the ceiling was not raised. The primary practical concern with a shutdown is the potential delay in the release of key economic data that informs the Federal Reserve’s decisions on monetary policy, including this Friday’s report on September payroll employment.

In a significant escalation of pressure on congressional lawmakers to head off a shut down, President Trump has instructed federal agencies and programs to make lists of non-essential workers whose positions could be eliminated. The federal employees most at risk work in programs which do not align with the Trump administration’s priorities. This means that once the shutdown is over, many of those furloughed workers may have no job to which to return if Congress does not agree to a deal to avoid a shutdown.

A mass firing of government workers would have a negative short term impact on the economy, depending on the extent of the layoffs. There is no way to know if this threat is real or just a negotiating tactic to force Democrats to make a choice between a reduction in government workers and using the budget battle and potential shutdown to boost spending on healthcare. Despite this threat from the President, the markets have largely ignored the potential shutdown as they historically are short in duration, and federal employees receive retroactive pay, becoming just a transitory blip on the economic radar.

Trade headlines came back into focus last week as President Trump announced on social media new tariffs on pharmaceuticals, large trucks, and selected furniture products to help achieve his goals of reviving domestic manufacturing and spurring the domestic production of patented drugs. The social media posts contained few details, and it is unclear what the impact would be given other treaties and exemptions that are in place. As we have stated previously, tariff threats will likely remain an issue for businesses and the stock market for the duration of President Trump’s term in office.

Look for a Moderate Acceleration in the Economy’s Growth Rate

It appears to us that the economy is beginning to emerge from a tariff-related stall and a series of forced adjustments since April. How long the process will take is unclear. Continued growth in earnings is important as companies that are growing earnings are not under pressure to cut jobs, allowing households to maintain their incomes and spending levels. While close to 150,000 federal government workers are set to roll off government payrolls this month, lower Treasury yields and the Federal Reserve starting a rate cutting cycle should support the economy into year end. The outlook for an acceleration in the economy’s growth rate following the mid-2025 stall remains on track. With the drag from the tariff hikes fading, energy prices lower than a year ago, ongoing efforts to lower regulations in certain sectors of the economy, and the Federal Reserve following through on additional rate cuts, the backdrop for the economy heading into 2026 should be positive.

Business capital spending incentives contained in the tax and spending bill signed into law last summer and a larger than normal level of income tax refunds from tax cuts retroactive to the beginning of 2025 will also provide the economy with a boost in early 2026, setting the stage for continued growth in earnings which should provide support for higher common stock prices.

Of course, just a general fading of policy uncertainty going forward should help provide a new steady state policy environment which can be relied upon and built upon, which would be broadly supportive of improved business confidence. Indications currently are that tariff-related pricing pressures are likely to be contained and market-based inflation expectations are consistent with inflation returning to the Federal Reserve’s 2% target over the next two years. Lastly, we remain optimistic about the long run given the inherent dynamics of the U.S. capitalistic economy to drive higher levels of earnings through innovation, creativity, self-interest to grow, and the desire for higher standards of living.

As September drew to a close, the nation faced another shutdown of the federal government -- 14 since 1981, many lasting only a day or two -- as lawmakers remained far apart on negotiations to pass annual funding appropriations for government agencies and programs. Under a shutdown, approximately 40% of federal employees (about 750,000) deemed “non-essential” would be furloughed and no federal employees would be paid until after funding is restored. In addition to permanently extending Affordable Care Act funding set to expire at the end of the year, Democrats are demanding to reinstate the cuts and changes to Medicaid that were part of the sweeping tax and spending bill signed into law last summer.

It is important to distinguish a federal government shutdown from an extension of the national debt ceiling which could result in a default on interest payments on U.S. Treasury securities if the ceiling was not raised. The primary practical concern with a shutdown is the potential delay in the release of key economic data that informs the Federal Reserve’s decisions on monetary policy, including this Friday’s report on September payroll employment.

In a significant escalation of pressure on congressional lawmakers to head off a shut down, President Trump has instructed federal agencies and programs to make lists of non-essential workers whose positions could be eliminated. The federal employees most at risk work in programs which do not align with the Trump administration’s priorities. This means that once the shutdown is over, many of those furloughed workers may have no job to which to return if Congress does not agree to a deal to avoid a shutdown.

A mass firing of government workers would have a negative short term impact on the economy, depending on the extent of the layoffs. There is no way to know if this threat is real or just a negotiating tactic to force Democrats to make a choice between a reduction in government workers and using the budget battle and potential shutdown to boost spending on healthcare. Despite this threat from the President, the markets have largely ignored the potential shutdown as they historically are short in duration, and federal employees receive retroactive pay, becoming just a transitory blip on the economic radar.

Trade headlines came back into focus last week as President Trump announced on social media new tariffs on pharmaceuticals, large trucks, and selected furniture products to help achieve his goals of reviving domestic manufacturing and spurring the domestic production of patented drugs. The social media posts contained few details, and it is unclear what the impact would be given other treaties and exemptions that are in place. As we have stated previously, tariff threats will likely remain an issue for businesses and the stock market for the duration of President Trump’s term in office.

The biggest risk to common stocks currently is the spring/summer stall in the economy deepening into a mild recession that leads to job cuts and weaker earnings, which could lead to additional job cuts as businesses attempt to protect profit margins.

The biggest risk to common stocks currently is the spring/summer stall in the economy deepening into a mild recession that leads to job cuts and weaker earnings, which could lead to additional job cuts as businesses attempt to protect profit margins. We see this risk as modest as the retail sales and consumer spending data for August point to steady household spending over the summer.

The credit markets are also not indicating any recession concerns as the yield spread on both investment grade and non-investment grade corporate debt is below the average yield spread. Specifically, the current yield spread on investment grade corporate debt is 75 basis points, while the average yield spread since December 1996 is 152 basis points. Likewise, the yield spread on non-investment grade corporate debt is 274 basis points, compared to the average yield spread since December 1996 of 542 basis points. We would be far more worried about the path ahead for the economy if credit yield spreads were running above their averages, but that is not the case currently.

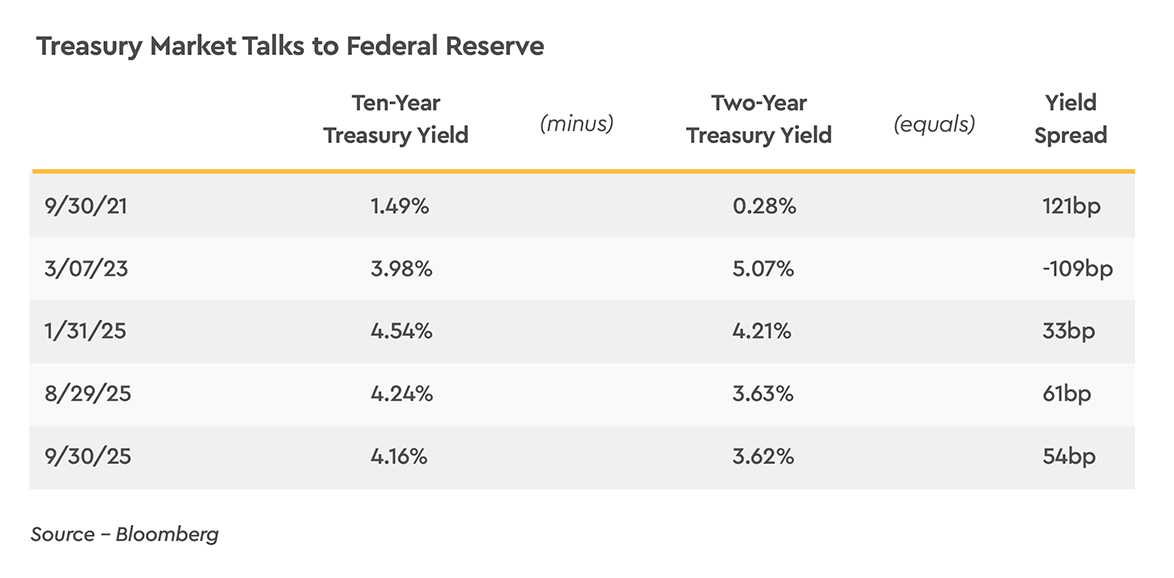

Similar to stock prices trading sideways to month end following the rate cut, yields on two-year Treasury notes backed up 11 basis points to end the month at 3.62%. Of the -63 basis point decline in two-year Treasury yields over the first nine months of the year, the real yield fell -106 basis points as investors acknowledged the recent stall in the economy’s growth rate and the expectation that the Federal Reserve is likely to cut rates further, while the two year inflation expectation rose 43 basis points as investors acknowledged the near term pricing pressures from tariffs.

Yields on ten-year Treasury securities have also fallen so far in 2025, ending 2024 at 4.58% and reaching a recent low following the rate cut at 4.01%. However, investors rejected the 4% yield level on the ten-year Treasury, with the yield ending September at 4.16%. Of that -42 basis point drop in yield over nine months, the inflation expectation rose a modest 3 basis points, while the real yield fell -45 basis points. It appears to us that the drop in real yield largely reflects a moderately better outlook for the federal budget deficit as tariffs are expected to add about $350 billion to the Treasury’s coffers on an annual basis. Tariff revenue does not solve the nation’s budget deficit imbalance, but it clearly helps.

Currently, the yield on two-year Treasury notes largely reflects the expected decline in the federal funds rate over the next couple months, on the order of 50 basis points. The two-year Treasury yield could decline further in 2026 as the one-time price increases from tariffs roll off the inflation data, and the nation’s underlying inflation rate resumes its descent to the Federal Reserve’s 2% target. We also assume the Federal Reserve will pursue a somewhat less restrictive monetary policy stance once the one-time, tariff-related pricing pressures are in the rear view mirror.

This outlook also assumes that President Trump’s appointee as the next chair of the Federal Reserve brings a pragmatic approach to the policy of setting interest rates and does not attempt to engineer a policy rate lower than that supported by the economic data. Additionally, we do not expect the yield on the ten-year Treasury note to trade consistently below 4% over the next few quarters, unless the economy’s growth rate disappoints in large measure from the expected 2% growth rate.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.

The credit markets are also not indicating any recession concerns as the yield spread on both investment grade and non-investment grade corporate debt is below the average yield spread. Specifically, the current yield spread on investment grade corporate debt is 75 basis points, while the average yield spread since December 1996 is 152 basis points. Likewise, the yield spread on non-investment grade corporate debt is 274 basis points, compared to the average yield spread since December 1996 of 542 basis points. We would be far more worried about the path ahead for the economy if credit yield spreads were running above their averages, but that is not the case currently.

Treasury Market

Treasury Yields Largely Unchanged During September, but Lower on the Year

Largely due to the stall in the economy’s growth rate starting in the spring and extending into the summer following the unveiling of President Trump’s reciprocal tariffs on April 2, Treasury yields have trended lower on the year, particularly at the shorter end of the yield. The two-year Treasury yield ended 2024 at 4.25% and reached a recent low at 3.51% on September 17 when the Federal Reserve resumed the rate cutting cycle, a decline of -74 basis points.Similar to stock prices trading sideways to month end following the rate cut, yields on two-year Treasury notes backed up 11 basis points to end the month at 3.62%. Of the -63 basis point decline in two-year Treasury yields over the first nine months of the year, the real yield fell -106 basis points as investors acknowledged the recent stall in the economy’s growth rate and the expectation that the Federal Reserve is likely to cut rates further, while the two year inflation expectation rose 43 basis points as investors acknowledged the near term pricing pressures from tariffs.

Yields on ten-year Treasury securities have also fallen so far in 2025, ending 2024 at 4.58% and reaching a recent low following the rate cut at 4.01%. However, investors rejected the 4% yield level on the ten-year Treasury, with the yield ending September at 4.16%. Of that -42 basis point drop in yield over nine months, the inflation expectation rose a modest 3 basis points, while the real yield fell -45 basis points. It appears to us that the drop in real yield largely reflects a moderately better outlook for the federal budget deficit as tariffs are expected to add about $350 billion to the Treasury’s coffers on an annual basis. Tariff revenue does not solve the nation’s budget deficit imbalance, but it clearly helps.

Currently, the yield on two-year Treasury notes largely reflects the expected decline in the federal funds rate over the next couple months, on the order of 50 basis points. The two-year Treasury yield could decline further in 2026 as the one-time price increases from tariffs roll off the inflation data, and the nation’s underlying inflation rate resumes its descent to the Federal Reserve’s 2% target. We also assume the Federal Reserve will pursue a somewhat less restrictive monetary policy stance once the one-time, tariff-related pricing pressures are in the rear view mirror.

This outlook also assumes that President Trump’s appointee as the next chair of the Federal Reserve brings a pragmatic approach to the policy of setting interest rates and does not attempt to engineer a policy rate lower than that supported by the economic data. Additionally, we do not expect the yield on the ten-year Treasury note to trade consistently below 4% over the next few quarters, unless the economy’s growth rate disappoints in large measure from the expected 2% growth rate.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.